{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

For many decades, manufacturing in the Middle East has been disproportionately concentrated in petrochemicals. The industry contributes 24 percent of GDP in Saudi Arabia and 16 percent in the United Arab Emirates (UAE), compared with less than 1 percent in the U.S. and China. Aside from light manufacturing activity—for clothing and processed foods, for example—Middle East countries import virtually all their manufactured products.

This high imbalance (the ratio of non-oil imports to non-oil exports is upward of two-to-one) presents risks that weaken resilience and could impede future economic growth in the region. In recent years, some countries—chiefly those in the Gulf Cooperation Council (GCC)—have launched ambitious programs to diversify and expand their manufacturing in order to meet national and regional demand, and to position the area as an export platform for companies based in other parts of the world. Typically these projects are implemented as part of a state-led master economic plan.

For governments pursuing these diversification programs, choosing which manufacturing sectors to target for development is critical. Technology is increasingly considered a high priority for localization compared with other manufacturing sectors, given its outsized importance to virtually every other industry, its growth potential, and the wide-reaching and adverse economic effects of supply disruptions. Within the vast technology universe, governments will have to place their bets on which tech segments—and even which product families within segments—to pursue with large-scale projects, and must provide ample support in order to ensure their success.

This report describes the state of manufacturing in the Middle East; the benefits of localizing technology manufacturing; and, for Middle East countries with ambitions to do so, the critical success factors.

The technology hardware manufacturing industry is highly concentrated geographically, with companies in a handful of countries functioning as providers to the world. For example, the Congressional Research Service estimated that in 2019, of the 126 semiconductor fabrication plants making 300mm silicon wafers, 36 were in Taiwan, 24 in China, 20 in the U.S., 19 in South Korea, and 13 in Japan—that is, 88.9 percent of such factories were in just five countries. Fabrication capacity is similarly concentrated, with 28 percent in South Korea, 22 percent in Taiwan, 16 percent in Japan, 12 percent in China, and 11 percent in North America—five locations accounting for 90 percent of the total.

Recently, several other countries and cities have created successful tech and digital manufacturing hubs, including Vietnam with electronics assembly (see “Samsung and Intel localize in Vietnam”); Grenoble, France, with microelectronics; and Vilnius, Lithuania, with laser technology. These regions and others increasingly recognize the value in having close access to a range of technologies, especially those that enable industrial innovation and digital transformation, and the supporting ecosystems.

In the Middle East, the UAE had a head start in pushing the localization agenda, with prominent players such as Mubadala investing in tech services including artificial intelligence (AI), cloud computing, space systems, and telecommunications.

More recently, Saudi Arabia has launched ambitious programs and megaprojects,6 which could further accelerate the technology and digital localization agenda.

The COVID-19 pandemic is expected to accelerate the localization trend as governments, regional authorities, and large manufacturers rethink their reliance on global supply chains and seek to bolster their resilience, especially in sectors such as semiconductors, whose components and finished products are critical to many other industries in-country.

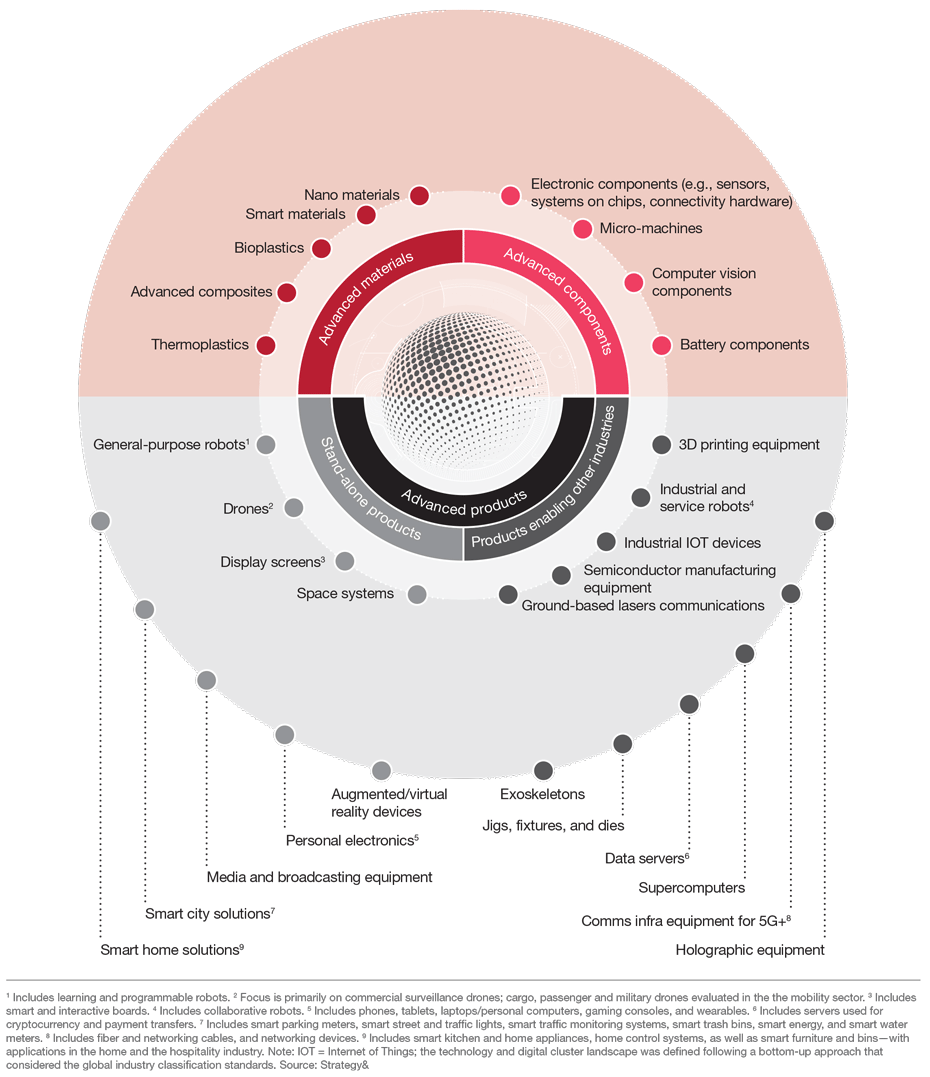

Governments can consider three groups of manufactured tech products—with a combined Middle East market size of roughly $125 billion, according to our estimates—for Middle East localization opportunities.

“Companies that invest significantly in R&D warrant special consideration; given the blistering pace of change in the tech industry, these companies are more apt to retain their leadership position and remain viable over the long term.”

Economic diversification is an imperative. The COVID-19 pandemic threw into sharp relief the region’s susceptibility to supply chain disruptions and challenged the region's resilience, making it difficult or impossible for companies to secure the technology on which they now heavily depend. Technology components and products are an integral part of modern-day economic and business activity. As competition intensifies to establish national tech manufacturing ecosystems and satisfy captive and global demand, Middle East country governments will need to move quickly to place their bets in those areas—materials, components, or products—where they have a right to win, and create the ecosystems to enable localized companies to launch and thrive.

{{item.text}}

{{item.text}}

Menu