Executive summary

Changes in the oil-field services and equipment sector in Saudi Arabia mean that both multinational corporations (MNCs) and their local partners need to review their strategies and approaches to partnerships. On the one hand, greater transparency and the easing of foreign investment regulations have made it easier for MNCs to do business in Saudi Arabia without the local partners that have traditionally acted as agents, distributors, or passive joint venture partners. On the other hand, a renewed focus on the localization of manufacturing and services presents an opportunity for local companies to support MNCs in establishing efficient manufacturing operations, or to position themselves as vertically integrated oil-field services and equipment suppliers.

The starting point is for local companies and MNCs to redefine their vision and strategy for engagement in the sector. They should take into consideration the characteristics of potential investments in the sector and assess how well their current portfolio and capabilities are aligned with the evolving requirements of the sector along two dimensions — localization potential and economic attractiveness. Local companies should then seek to determine how their existing marketing, supply chain, and support service capabilities can be further developed to enable the localization of manufacturing. In addition, local companies that wish to play a more active and sustainable role in the oil-field services sector need to ensure that they have the financial wherewithal to co-invest with their MNC partners or to invest in their own capabilities.

Local companies that proactively develop and adapt their capabilities will be best positioned to retain their existing partnerships and attract new MNC partnerships. Alternatively, they can become independent suppliers of oil-field services and equipment.

A more open investment regime

Increased transparency and greater openness to foreign investment are making it easier for MNCs to do business in Saudi Arabia without local partners. Saudi Arabia has progressively relaxed foreign investment regulations since 2000. These changes have included revisions of key pieces of legislation, along with the formation of the Saudi Arabian General Investment Authority (SAGIA), whose mission is to “develop and attract investments by improving the investment environment.” The accession of Saudi Arabia to the World Trade Organization in 2005 further reflected Saudi Arabia’s commitment to reforming and liberalizing its economy.

In particular, recent changes have the potential to make partnerships redundant, especially for large, well-established companies. In September 2015, SAGIA announced that non-Saudi entities would be permitted to own 100 percent of wholesale and retail operations, subject to certain conditions. These conditions include commitments on inward investment, the training and employment of Saudi nationals, manufacturing 30 percent of distributed products locally within five years, investing 5 percent of gross sales revenues in local research and development, and establishing Saudi-based logistics and after-sales support operations. In response, a number of large foreign companies, such as Dow Chemical, Pfizer, and 3M, have obtained licenses to conduct trading activities through wholly owned companies.

Of course, partnerships remain an important option for smaller foreign companies that have less international experience or for new entrants to the Saudi market. For such companies the establishment of an agency or distributorship is common practice because it allows them to understand market dynamics and mitigate risks.

A renewed focus on localization

Saudi Arabia has long had a policy to localize manufacturing activities and create employment, a policy whose recent renewal provides an incentive for MNCs to seek local partners or for local firms to become independent oil-field services and equipment suppliers. There have been previous initiatives, such as Nitaqat from the Ministry of Labor, which was introduced in 2011 to encourage the employment of Saudi nationals through incentives and penalties. However, official efforts at localization have often met with limited success because of the absence of a cohesive national strategy for local content development; uncoordinated local content development efforts lacking a single, empowered coordinating entity driving the agenda; incomplete monitoring, regulations, and enforcement of local content objectives; and, procurement practices that limit the ability of local companies to participate and compete.

The decline in oil prices since mid-2014 has provided a new urgency to diversify the Saudi economy away from oil. Saudi Vision 2030, announced in April 2016, emphasizes the maximization of local content, job creation, and private-sector participation. To support these objectives, a Local Content and Private Sector Development Unit was formed within the Council of Economic and Development Affairs in December 2016. This unit’s task is to increase local content, support the development of the non-oil private sector, and improve the balance of payments. The unit plays an important role addressing barriers to localization across different industries, such as through the establishment of industrial zones and reviewing import tariffs.

For oil-field services and equipment specifically, the key localization initiative is Saudi Aramco’s In-Kingdom Total Value Add (IKTVA) program, launched in December 2015. IKTVA is solely focused on the oil sector and so can have an important effect on oil-field services and equipment partnerships. As the sole buyer for the majority of oil-field services and equipment, Saudi Aramco is in a unique position to directly influence the localization strategies of key suppliers. IKTVA’s objectives are to:

- Double the percentage of locally produced energy-related goods and services from 35 percent in 2015 to 70 percent by 2021

- Export 30 percent of output from the local energy goods and services industry

- Create half-a-million direct and indirect jobs for Saudi nationals

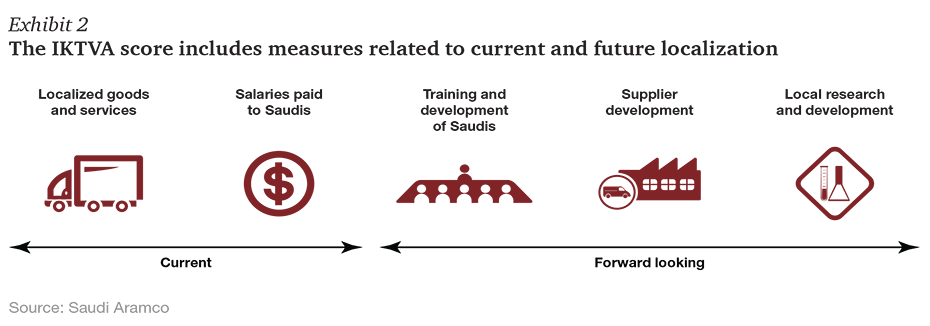

Saudi Aramco is placing increasing emphasis on IKTVA in the award of major contracts. The company’s top 100 suppliers are subject to an audit procedure that generates an IKTVA score based on measures of current localization (expenditure on local goods and services, and salaries paid to Saudi nationals) and forward-looking measures that demonstrate how the supplier is supporting future localization (training and development of Saudi nationals, supplier development, and local research and development) (see Exhibit 2). Saudi Aramco works with suppliers to ensure that actions taken are aligned with national objectives. The resultant IKTVA score is used to determine the contract award.

Although the IKTVA program is still developing, it is already having an impact. Saudi Aramco reports that locally produced energy-related manufacturing accounted for 43 percent of the total in 2016, up from 37 percent in 2015. In addition, the IKTVA score was a key component in the process to select suppliers for contracts that could total over SAR 60 billion (US$16 billion).1 Meeting IKTVA targets to remain competitive is forcing companies to rethink their supply chain operations so that they switch to local suppliers and develop the local supply chain wherever economically justified.

Companies do not have the luxury of waiting to see how the final IKTVA approach develops. They need to take action now. Indeed, Saudi Aramco, through the agency of IKTVA, requires that MNC suppliers deliver a clear road map for increased localization. In developing these road maps, MNCs will need to consider their existing partnerships, and consider the roles that current and future local partners may play in helping them to achieve cost competitiveness and profitability for localized manufacturing operations.

Conclusion

Although the investment landscape in Saudi Arabia may seem worrisome for local companies, the current changes herald the start of the next phase of development of the oil-field services and equipment sector. In this new era for partnerships, success will come to MNCs that can leverage local partnerships to drive increased localization, and to those local companies that can offer the capabilities to support this process. The changing environment offers important opportunities to those local companies that proactively align their strategy and capabilities to meet the new requirements. Local companies that succeed in developing their capabilities will emerge as partners of choice for MNCs or as independent local suppliers.

1 In-kingdom Total Value Add (iktva) — program in motion, Saudi Aramco, 2016.

Contact us

Menu