Executive summary

Freight transportation and logistics (T&L) is a critical industry for the Gulf Cooperation Council (GCC)1 countries, yet its technology and infrastructure lag behind that of developed countries. Worldwide, new digital tools and applications are transforming T&L at all stages of the value chain. GCC companies have not seized this opportunity, nor capitalized on these technologies — which they must to remain competitive with global players. Digital is more than a tool to improve efficiency — it is a means to fundamentally rethink business models and better support national goals of creating more vibrant economies.

There are numerous emerging technologies relevant to GCC T&L players. Many of these technologies are still in the initial stages of implementation. They have a long way to go in terms of regulatory support and capability development within companies before they are commercially viable. Nonetheless, several are further advanced and should be at the top of GCC T&L companies’ strategic agendas: big data and analytics, on-demand mobility, and blockchain.

We have observed that these digital solutions have the potential to reduce operating costs by 10 to 30 percent and reduce operational risk and breakdowns by up to 75 percent. Even more compelling is that these technologies allow T&L companies to develop new business models, based on services that dramatically improve customer engagement and unlock new revenue sources.

To capture these gains, GCC companies must move fast or risk ceding the first-mover advantage to their competitors. Already, some early adopters are implementing these technologies and retooling their operations and offerings, leading to operational and financial performance gains. To succeed, companies must apply a framework in which they rethink their strategic objectives and business model and then define a digital strategy to address their business needs.

Challenges could lead to a critical opportunity

The T&L industry in the GCC faces a combined, existential threat of declining business and outdated infrastructure. At the same time, T&L companies have a critical, once-in-a-generation opportunity to implement digital technologies that can transform their businesses.

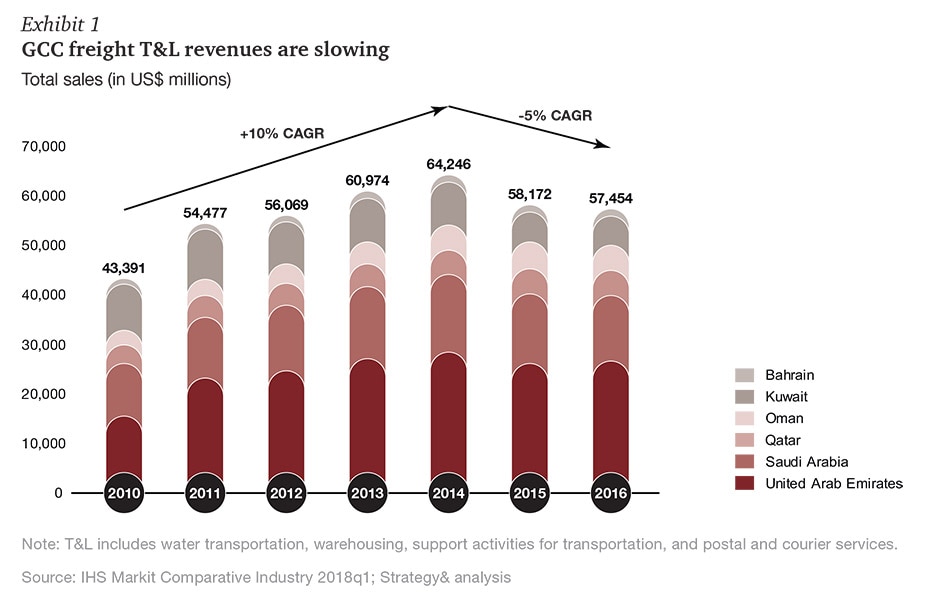

From 2010 through 2014, freight revenue in the region grew at a steady pace of about 10 percent. Since then, revenue has declined by about 5 percent a year, due to slowing economic activity in the region (Exhibit 1). As oil prices remain low, businesses are scaling back projects, imports are down, and governments are spending less on the kind of infrastructure projects that require major freight shipments.

In addition, the region’s T&L industry significantly lags behind its global peers in terms of technology. T&L is a latecomer to digitization, with many management teams still applying an analog mind-set. It is a traditional industry worldwide, dating back to the origins of commerce. The Strategy& Industry Digitization Index, which looked at how various sectors use data and analytics to improve operations, found that T&L is behind utilities. Based on our experience, GCC T&L companies are less digitized than their peers in more developed markets.

The slow progress thus far is not due to a lack of options. The industry is witnessing a wave of innovation across the entire value chain, as startups emerge with new, intelligent solutions to solve the challenges of moving goods across land and sea. To date, most GCC companies have not adopted these solutions — a critical failing that puts them at a steep competitive disadvantage, with no chance to recover.

The industry’s cautious approach poses the risk that technology could be imposed on T&L because of the dynamics that are reshaping other sectors. If T&L companies continue to take the back seat in exploring and investing in new digital solutions in alignment with their overall business objectives, then they could instead end up with unplanned and inefficient technology retooling that is designed for the benefit of other firms. For example, in March 2018, Authentag, which provides inventory management services, announced that it will introduce a blockchain-based ledger system for the pharmaceutical industry to provide tracking and verification services for products. Successful trials for similar systems could force the T&L sector to adopt them to cater to the business needs and requirements of its large corporate clients, whether or not these technologies fit with any particular T&L company’s needs.

The policy environment, however, should encourage the digital transformation of GCC T&L. Governments in the region are making large-scale investments in digital to promote sustainable economic growth. Saudi Vision 2030, for example, seeks to increase the private sector’s role in the economy and diversify away from dependence on oil. Critically, it aims to improve logistics throughout the country. The United Arab Emirates (UAE) has an even stronger focus on T&L. The UAE Vision 2021 sets goals for innovation, including making digital technology one of seven primary national sectors, and it aspires to make the country first overall in the global rankings of air transport and port infrastructure, and among the top 10 in terms of logistics. For these broad initiatives, investing in T&L is a short-term goal and a means of hitting more ambitious economic targets. Moreover, digital investments in the region are low risk as they involve retooling and redesigning minimal amounts of legacy IT infrastructure.

Conclusion

To date, many T&L companies in the GCC have resisted investing in technology, but that wait-and-see mind-set now threatens to render them irrelevant. Digital tools and applications are advancing rapidly, and T&L companies in other markets are already capitalizing on them. T&L executives in the GCC need to start taking action today. If not, they will serve as a drag on the region’s economic aspirations, rather than an engine to help achieve them. More important, a failure to embrace digital will put T&L companies themselves at a permanent disadvantage — one from which they will not recover.

1 The GCC countries are Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

Contact us

Menu