{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Download PDF - {{item.damSize}}

Chris Bartlett, Zia Bhadiar

February 7, 2019

Commoditisation poses an increasing challenge for the telecommunications sector globally. Australian operators, which have been relatively successful in resisting this trend, have begun to feel its impacts in recent years. Confluence of market trends such as the proposed consolidation of the mobile operator market, the increase in price-based competition and the growth of the budget segment are placing increasing pressure on average revenue per user (ARPU), industry profitability and the sustainability of the traditional operator business model.

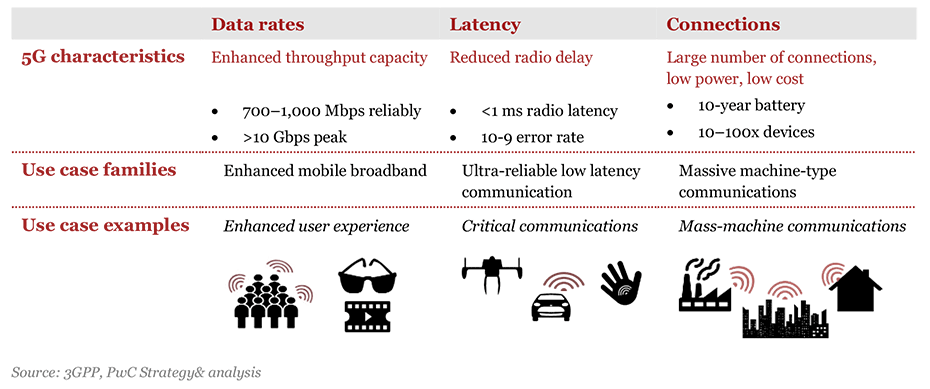

The market outlook is further complicated by the emergence of fifth-generation mobile network (5G) technology, which promises to revolutionise telecommunications by providing differentiation options through ‘futuristic’ digital use cases. While these use cases may ultimately transform the way we use technology, the first set of 5G standards only focuses on ‘enhanced mobile broadband’, and it is unlikely that operators will be able to offer ultra-reliable, ultra-delay-sensitive and massive machine-type communication products for at least another three to five years. Considering the long investment horizon and competitive dynamics in the supplier market, there is a significant degree of hype contributing to unrealistic expectations across the board.

Given the uncertainty surrounding the technology, operators’ perspectives on the future of 5G vary widely, with some being sceptical and others highly optimistic. Most will agree that the opportunities presented by 5G require careful strategic planning in order to capitalise on the potential for greater differentiation and value capture in the future.

As such, this paper reflects our perspective on five of the key concerns facing operators

a. Do we really need 5G? What can’t we do with 4G? From a technical perspective, 5G technology is only an incremental change to 4.9G, the latest version of standards for 4G. Adding to this, most 5G use cases can be implemented with 4.9G, and only a handful of the truly 5G-enabled use cases require nationwide coverage. This supports the case to further invest in 4G and sweat existing assets as customer requirements and adoption mature. We expect value from any near term investment in 5G to be derived from marketing claims related to having a ‘superior’ network and seeding innovation across the sector.

b. Will 5G help lift consumer and enterprise revenue? Consumers demand differentiated services when paying premium prices, and historically have been unwilling to pay more simply for better broadband. New ‘experience -based’ consumer value propositions (e.g. gaming packs) will need to be developed by leveraging network slicing and mobile edge computing features in 5G. In addition to differentiated services, 5G’s efficiency and capacity could allow operators to develop viable consumer offers for fixed-mobile substitution and unlimited data plans to price sensitive segments. In the enterprise segment, operator success depends on understanding where and how to play, and choosing verticals that align with business strengths. In Australia, we can see that the construction, mining, healthcare, agriculture and manufacturing sectors are set to benefit most from the Internet of Things (IoT) and 5G.

c. Can 5G help us bring down the cost per MB? 5G is expected to drive material efficiency gains due to its higher data capacity, allowing operators to reduce the relative cost base and increase competitiveness in the market. However, these gains depend on a compatible device ecosystem, which will require higher 5G device penetration and timely product launches by handset vendors, especially Apple for the Australian market, and this will not happen until late 2020.

d. Do we have the right size and type of spectrum for 5G? Operators should ideally have 80–100 MHz in the Mid Band, which is most popular since it can be deployed directly onto their current mobile tower sites to replicate 4G coverage at a higher capacity. In the High Band, which will be predominantly used for small cell, hotspot and industrial 5G deployment due to its limited propagation characteristics, operators should ideally have 800–1,000 MHz. Timely access to the appropriate spectrum is expected to be key to success for 5G, as a robust spectrum strategy becomes increasingly critical.

e. 5G will blow up our capital expenditure (capex) envelope! Can we really afford it?Analysis suggests the capex ratio of operators should not materially change with the introduction of 5G, based on the likely deployment models. Upgrading mobile tower sites, deploying small cells in high-density areas and eventually rolling out 5G nationwide could potentially be done within the existing capex envelope if staged carefully over the next five to seven years.

5G may provide considerable opportunities by revolutionising services, products and experiences – and eventually the whole ecosystem. However, the ‘right to win’ in the brave new world of 5G will be taken by operators that are proactive and develop a holistic approach to:

5G technology characteristics and application categories

We recommend a pragmatic four-step approach to deliver on the above objectives:

i. Operators need to start early by looking at how their current 4G technology could allow them to deliver most use cases, building momentum and being ready to scale with 5G.

ii. The key here is not going after the whole market but for operators to pick the segments or verticals where they have the strongest internal capabilities, external ecosystem and customer relationships.

iii. Operators need to design innovative business models that reflect the changing nature of value created and delivered to customer segments through 5G.

iv. Finally, operators should select the right partnership model to extend beyond connectivity in the 5G value chain and access new and greater value pools.

5G represents a significant opportunity for innovation and differentiation. It is key for operators to plot their path forward in a sustainable way that optimises their ROI and builds on capabilities they will need in the future.

Download PDF - {{item.damSize}}