Executive Summary

As of May 2020, Japanese insurers have mobilized rapidly in response to the COVID-19 pandemic. The sudden decrease in global interest rates and significant restrictions on people’s movement are necessitating changes to product portfolios, distribution models, and business operations.

However, business continuity and crisis management are only half the story; while there is a pressing need to react quickly to fast-moving events, insurers must also reassess their long-term strategy. The need for establishing customer trust and supporting them through a time of need has rarely been greater.

We expect the market to be significantly different over the longer term and here is what insurers should focus on:

- Evolve product portfolios to reflect lower interest rates and changes to underlying risks—this extends to optimizing underlying investments (to achieve the desired yield) as well as extending into adjacencies to capture new revenue streams

- Become digitally enabled across customer interactions, distribution (including agents/ banca partners), core operations, and back-end processing to support new ways of working and evolved risk profiles

- Integrate more tightly with suppliers to support their customer promise—in the short run, this means working with them to creatively support their businesses.

- Rethink the operating model—beyond organization structures and processes, successful insurers will critically rethink their workforce strategies, cost structures, physical presence, and organizational culture to build resilience and adaptability.

The successful insurer of the Post-COVID era will be the ones that take a holistic approach to rethinking their business (beyond just reacting to market dynamics).

Insurers can move in this direction by calibrating their mid- and long-term strategies around six key areas: strategy & brand, distribution, finance & liquidity, workforce, operations & supply chain, and being proactive about the regulatory agenda. In short, insurers must watch the immediate situation,but with a firm focus on the emerging future to deliver on customer promises and stakeholder expectations.

Impact of COVID-19 on Japan

As of May 2020, Japanese insurers have mobilized rapidly in response to the COVID-19 pandemic. For insurers who have predominantly relied on face-to-face (F2F) distribution and people-intensive operations, the battleground extends to all fronts: mass customer acquisition, running the business, and delivering on claims.

Domestic sales have declined significantly because insurance agents are unable to meet with customers and reduced discretionary spending given the possibility of unemployment.

While the impact to date on general insurers is less pronounced, few expect this trend to continue. If the experience of other regional markets is any indication*1, Japanese insurers should expect a double-digit decline in new businesses in the initial months of the restrictions and a low, single-digit reduction in annualized premium income thereafter. Several insurers have started making regular compensatory payments to their agents*2, further impacting profitability and liquidity. Market volatility and declining interest rates have challenged investment portfolios and overseas business interests further.

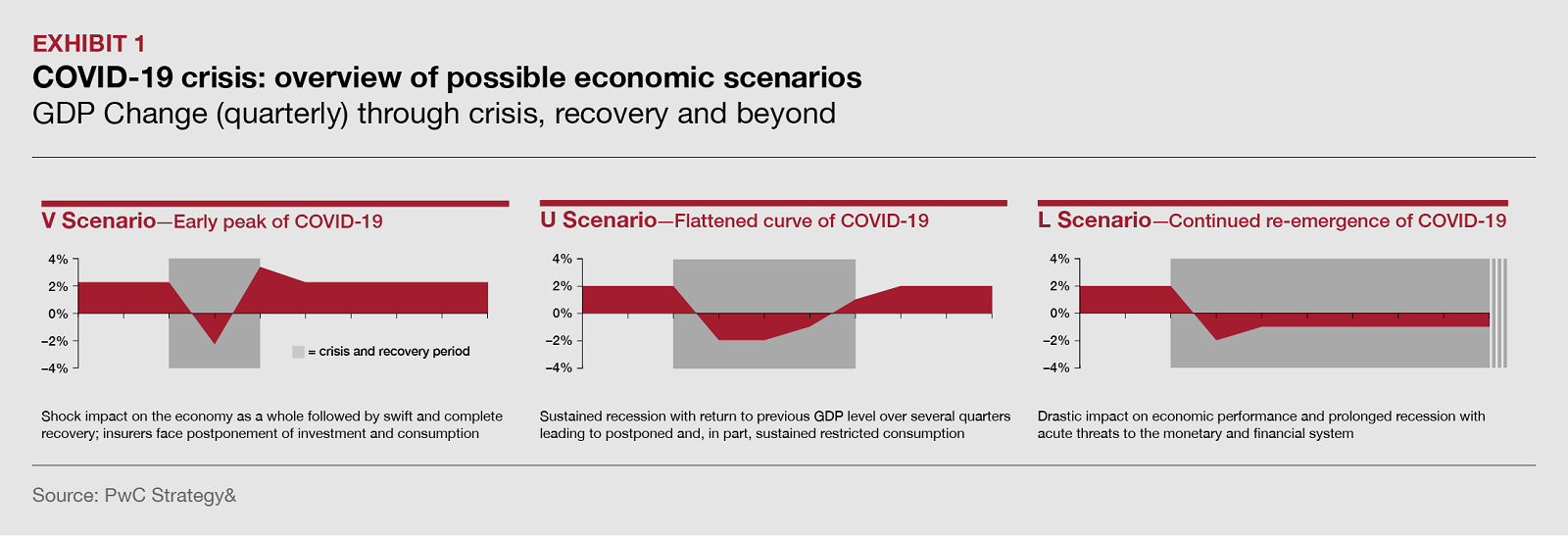

Yet, a relentless focus on business continuity will only get you so far—insurers need to have one eye on the future to emerge strong and capture the significant market opportunities that emerge. In this context, we see three broad scenarios developing over the next ~12–18 months, both globally and in Japan outlined in the figure below (Exhibit 1).

Our house view is that scenarios U and L are most credible and insurers will need to adapt accordingly. After crisis management, as national governments gradually pull societies out of hibernation, opportunities will arise for insurers who act now to position themselves to emerge stronger in the post-COVID times. To respond effectively, Japanese insurers need to cater to four Japan-specific issues:

- A significant shift toward remote working

- Regional variances in COVID related economic impacts

- A higher degree of manual operations vis-à-vis global peers

- Improve governance of their global portfolios

*1: Insurance Journal, 2020. “Hong Kong Insurers Say Sales Have Fallen to ‘Almost Nothing’ Due to Coronavirus”, Accessed June 30, 2020.

Global Data., 2020. “South Korea’s life insurance business to decline in 2020 due to Covid-19, says GlobalData”, Accessed June 30, 2020.

*2: Top 5 Japanese insurer announcement

The title and title of the author in the PDF file is at the time of writing this report.

Contact us