Shifting toward a noble purpose

A low interest rate environment notwithstanding, Japanese insurers are among the most profitable (and largest) in the world. Japanese consumers have some of the highest rates of insurance ownership in the world and their longevity yields large value pools. Health (i.e., the third sector) is also an area that continues to grow and in which margins remain attractive.

Despite all these favorable trends, few insurers have managed to embrace the customeragenda. None have been able to go beyond a transactional service to build trust with the customer toward a noble purpose: supporting customers through their toughest times.

Changes in customer expectations, digitalization becoming mainstream, emergence of new business models, and step changes in analytical approaches present a unique opportunity for insurers—an opportunity to move beyond selling basic protection to engage more deeply with and provide solutions for the customer.

To capture this opportunity, however, requires insurers to think differently about their purpose, who they want to be, and how they should participate in the market.

This paper examines the changing issues in the life insurance industry and presents a capability model to help insurers succeed in the Japanese market. In addition, we will identify the four “minimum required” capabilities that are critical for achieving results through competition in the life insurance market and alleviating business and structural issues. We also present the conditions for becoming a successful insurer in the future.

The Changing Customer

The customer base for the Japanese life insurance industry is heavily influenced by three distinct trends: a fundamental change in demographics, emergence of health as an area of worry, and secular increases in digital attitudes.

The aging population is reshaping longevity risk and needs for solutions. By 2040 there will be an extra ~10m people over the age of 65 even as the total population decreases by ~20m. Over the same period, population concentrations in Tokyo will continue to increase (at the expense of rural Japan) and female participation in the workforce will climb to~45+%. These changes will have a profound impact on distribution footprints and underlyingeconomic models.

Increasing life expectancies and the rise of lifestyle-related ailments are also contributing to increasing awareness about health. In the coming years, ~30%+ of the population will be obese with a B+B2 25+ and ~3m citizens will suffer from chronic illness. Amidst all of this, many service providers are emerging (diet, digital health, fitness, preventative medicine, etc.) and Japanese consumers’ spending on health and wellness is estimated to reach JPY10 trillion. Unfortunately, none of this is being spent with insurers.

Lastly, customers are changing how they engage with insurers. Across age groups, the portion identifying themselves as digital natives tripled from 7% in 2010 to an estimated ~21% in 2020. Another recent PwC Japanese consumer survey indicated that insurance customers are willing to pay 7% more for a superior experience, and 50% of the same group indicated the need for continued human interactions. Experience matters, and more than ever before, it is about blending digital and physical.

New Battlegrounds – The Convergence of Life, Health & Wealth

On a national level, healthcare expenditure has continued to grow—the combination of public spending on health, voluntary schemes, and out-of-pocket spending is up more than 50% over the last 15 years. Based on our research, out-of-pocket spending on health-related services in Japan is estimated at $150-$250b p.a. and growing quickly. As public finances become more challenged, customers will inevitably have to pay for an increasingly larger share of health-related spending.

In parallel, wealth management is emerging as an area of unmet customer needs. The average age of retirement has not kept pace with the higher life expectancy, leaving customers to fund longer retirement periods. Furthermore, over 70% of retirees’ assets are in cash (yielding very low returns). Existing players (mostly fund managers and securities firms) are not meeting customers’ needs—performance remains volatile and fees paid by Japanese customers are among the highest in the world. Against this backdrop, there is a genuine opportunity for insurers to support customers.

Insurers are unique in that they typically have long-lasting customer relationships, as customers trust them to be around at times of need and strong agent-customer relationships often span multiple years. Insurers have privileged access, and this gives them a right to play in the wealth management arena at a time when the issues that retirees are most concerned about deal with health and wealth.

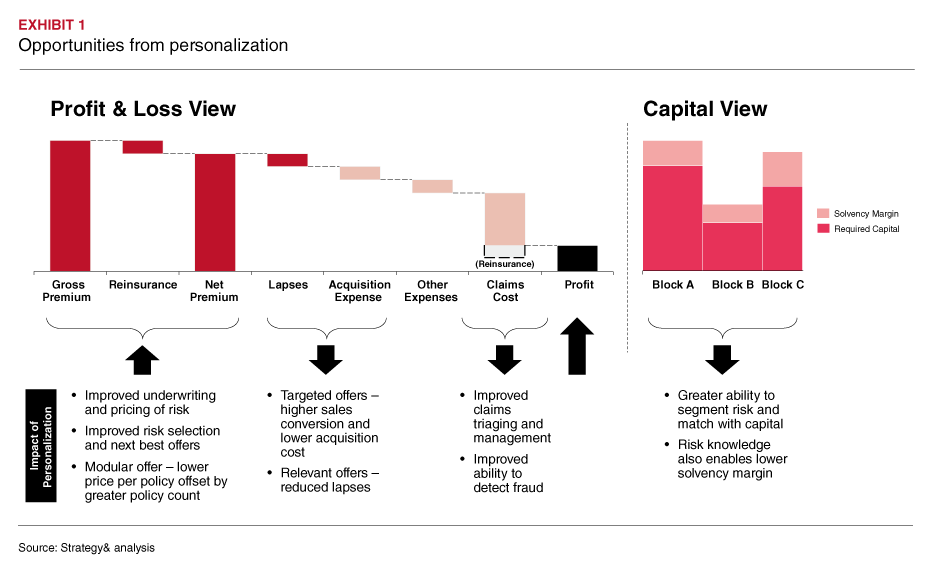

Predictive and Personalized

Since its founding, insurance has been about underwriting the whole pool of risk and many of the processes have been focused on ensuring the “right” pool—for example, underwriting was designed to filter out bad risk such that it met the assumptions that went into defining the pool of risk being insured. This is particularly true in markets like the third sector in Japan, where profitability has historically been driven by scale and managing to average the incidence rates of certain diseases.

However, the evolution of analytics technologies and mainstreaming of experiences as a differentiator mean that an average based business is no longer sufficient. Increasingly, the successful insurer of the future will be the one that is able to use analytics and design to deliver a predictive, personalized experience to customers. With this personalization, there is an opportunity for insurers to tackle the structural drivers of profitability and capital efficiency inherent in their business.

The title and title of the author in the PDF file is at the time of writing this report.

Contact us