{kind=link}

{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Download PDF - {{item.damSize}}

Life sciences, and pharmaceutical companies in particular, are an important pillar of the U.K. economy. The life sciences sector turns over almost £50 billion per year, employs 175,000 people, and boasts almost 5,000 active companies. Its economic contribution is substantial, but its positive impact goes beyond that, being a source of innovation, skills, and competitive advantage. Hence the support the sector receives from the U.K. government, which has a dedicated minister for life sciences, supported by the government’s Office for Life Sciences.

Cambridge, London, Oxford, and the South East of England are the U.K.’s powerhouse for life sciences. All of the world’s top 20 pharmaceutical companies have invested in this region, which boasts three of the world’s top 10 universities (Oxford, Cambridge, and Imperial), a variety of other top-quality institutions, and a thriving life sciences sector. Japanese pharmaceutical companies already play an integral part — between 2005 and 2014 they were the second-largest contributor to foreign direct investment for life sciences in the region.

MedCity is a London-based collaboration between the Mayor of London and London’s three academic health science centres, working with University of Oxford and Cambridge University, to promote and enhance life sciences in the sector. MedCity commissioned this report to find out what is attracting Japanese companies to the Cambridge, London, Oxford, and the greater South East of England, what factors might encourage more to come here, and what action could be taken to make the South East of England an even better option than other locations.

The findings in this report, having been substantiated by interviews with Japanese pharmaceutical companies, identified three key factors: access to an abundance of talent, a good IP & legal framework, and a strong and diverse life sciences ecosystem:

As this report shows, these factors have already attracted substantial inward investment from Japan. However the report highlights areas where Japanese companies in the region see possibilities for improvement. These range from a reduction in red tape to establish clinical trials and integration into the NHS, to venture capital to foster incubators of innovation that Japanese companies can later access.

MedCity, its partners, and its stakeholders in the life sciences fields are taking on these challenges. Everyone has a role to play to ensure we achieve maximum benefit for all involved in Japanese investment in the South East of England, and the significant opportunities it presents.

I hope you enjoy reading this report and that it stimulates dialogue as to how the Japanese life sciences community can better collaborate with Cambridge, London, Oxford, and the South East of England.

Eliot Forster

Chairman of MedCity

Life sciences is an important sector of the U.K. economy, and it is expected to be a major contributor to the country’s long-term economic development. A number of government-supported life sciences initiatives have been launched in recent years, including the new Precision Medicine Catapult launched this year in Cambridge, the Cell Therapy Catapult in London, Leukaemia & Lymphoma Research’s Trial Acceleration Programme in Birmingham, and the 100,000 Genomes Project run by Genomic England. There are also a number of academic, healthcare, and industry consortia forming across the country, including MedCity, launched in April 2014; the Northern Health Sciences Alliance, launched in May 2014; and 15 academic health science networks and seven academic health science centres.

The U.K. has a strong presence within all three of the industry subsectors: pharmaceutical, medical technology, and biotechnology. According to the Bioscience and Health Technology Database1, there are nearly 5,000 life sciences companies in the U.K. that develop, produce, and market products and services across these three subsectors. Almost 10% of these are in pharmaceuticals, and all of the global top 20 pharmaceutical companies are active in the U.K., with most of them in the South East of England (SEE). This is evident in cities such as Oxford, where three of the top six European Union–based biotechs have an HQ2.

Japanese companies are an important investor in the U.K.’s life sciences industry, especially in pharmaceuticals. A recent joint study by MedCity and London & Partners3 found that between 2005 and 2014, Japan was the second-largest4 contributor to foreign direct investment (FDI) for the life sciences sector in the Greater South East; projects ranged from sales and marketing, to R&D, to establishing new commercial bases. Of a total 336 FDI projects in the region, 33 were sponsored by Japanese companies (10%). These 33 projects contributed to the creation of 1,504 jobs and £163.7 million in capital expenditure. Pharmaceuticals was by far the most important subsector for Japanese FDI, accounting for 24 projects (73%) and 1,377 jobs (92%).

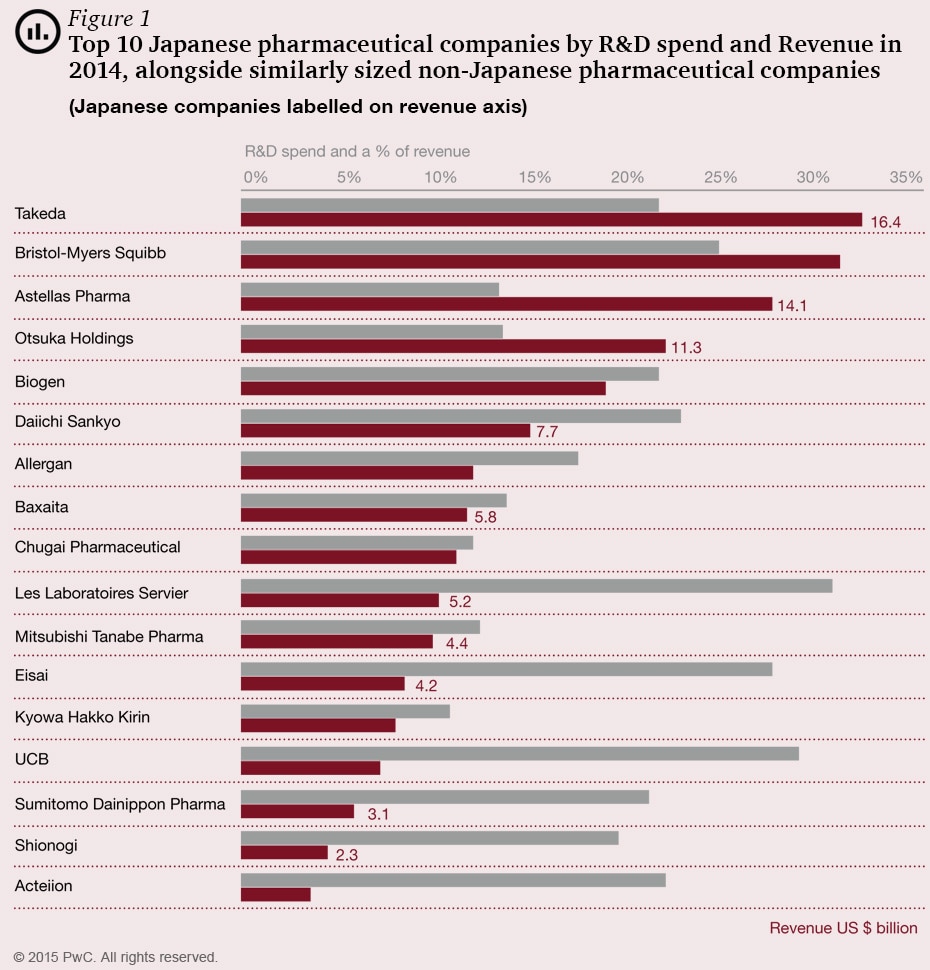

The Japanese pharma industry is looking to grow by expanding overseas. In 2014, Japan initiated more overseas investment projects than any other nation in Asia-Pacific, and the £33 billion of capital it invested abroad was second only to China (£42 billion). The Japanese pharmaceutical sector, in particular, has more than enough capacity to make significant overseas investments: R&D spending by Japanese research-based pharmaceuticals amounts to only 11% of their sales, compared to 17% in the E.U. and 21% in the U.S.5 A recent report by Evaluate Ltd shows that 11 of the world’s top 50 pharmaceutical R&D investors are based in Japan (22%) yet they account for 12% of R&D spending6 (see Figure 1). Generally, Japanese pharmaceutical companies have also accumulated large cash reserves, and are looking for new investment opportunities. By way of example; in 2014 the top 3 global pharma companies held, on average, cash and equivalents worth 13% of revenue — the top 3 Japanese companies held 28% worth of cash and equivalents.7

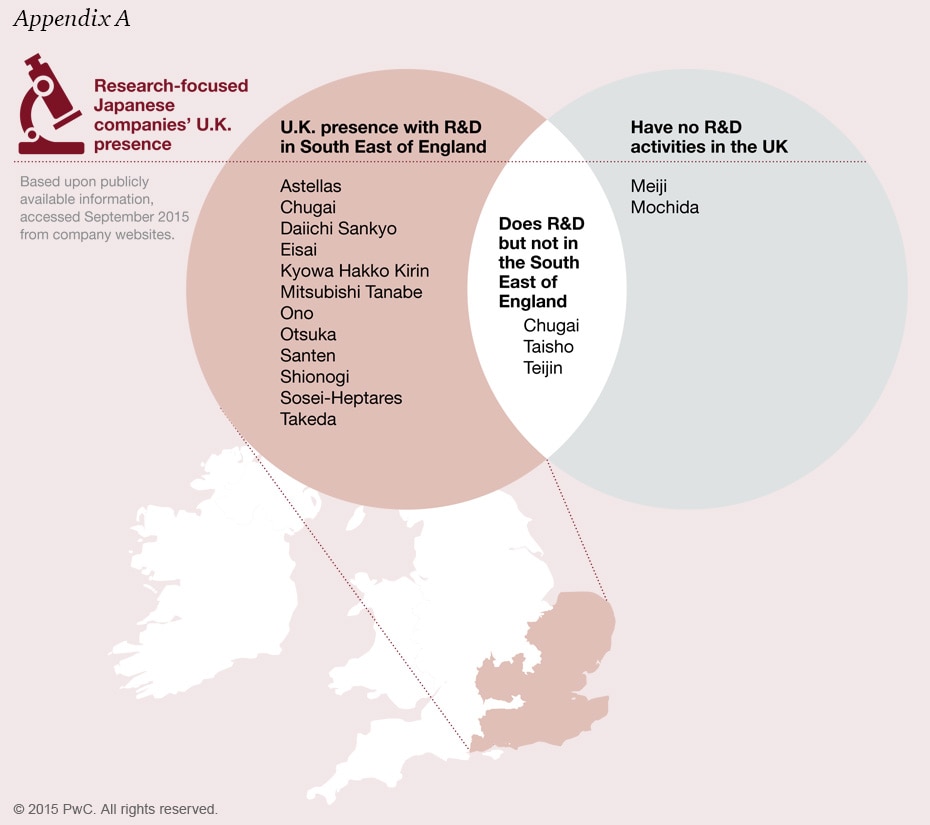

Simultaneously, as international expansion is becoming more attractive for Japanese companies, it’s also getting significantly easier. Recent government reforms have made considerable progress in harmonising Japan’s domestic regulations with those in the E.U. and U.S. This is accelerating more investment within the Japanese pharmaceutical sector, both inward and outward, as Japanese companies look for potential acquisitions. Many of these businesses looking overseas for new opportunities are finding them in the U.K. And of the 13 Japanese pharmaceutical companies that have a presence in the U.K., 12 are based in the SEE region (see Appendix B).

So what is attracting Japanese companies to the South East of England? What factors might encourage more companies to come here, and what action could be taken to make the region a better option than other locations? These are the questions our report addresses.

In 2014, Japan initiated more overseas investment projects than any other nation in Asia-Pacific.

The Greater South East region is the powerhouse for the life sciences industry in the U.K.

It offers substantial attractions to Japanese companies looking to locate overseas, from the quality of its talent and academic institutions, to the robustness of its regulatory framework, to the diversity of the pharmaceutical sector. Add to that an open and positive society, the availability of both specialist and general management talent, and competitive costs, and it’s clear the region has a vast number of opportunities to offer.

The challenge is to communicate these benefits more widely to the Japanese life sciences sector, and to ensure action is taken in certain specific areas, to address the relatively minor factors that are currently impeding further inward investment by these businesses. Such steps should be aimed at reducing red tape and increasing support for innovation.

Taken overall, this is a significant opportunity, and one which is well within grasp.

1 The Bioscience and Health Technology Database is funded by the U.K. government, and its role is to collate information on the medical technology, medical biotechnology, industrial biotechnology, and pharmaceutical companies in the U.K.

2 Labiotech, 15/09/2015. Immunocore, Oxford Nanopore, and Adaptimmune.

3 ‘Understand the Life Sciences Cluster from an Inward Investment Perspective’, MedCity and L&P 2015’. Study focuses on Jan. 2005 – Dec. 2014.

4 Japan was second only to the U.S.A. in their life sciences FDI contribution.

5 IFPMA, The Pharmaceutical Industry and Global Health, Facts and Figures 2014.

6 2014 Pharma R&D Ranking, Evaluate Ltd. The Japanese 22% of the top 50 accounted for 12% of the top 50’s spend: US$13.1 billion. It is worth noting in the last three years (mid 2012 – mid 2015) the yen has depreciated by approximately 35% against the U.S. dollar, suppressing the market size during international comparisons.

7 Top 3 global pharmas by 2014 R&D spend; Pfizer, Roche, and Novartis. Top 3 Japanese pharmas by 2014 R&D spend; Takeda, Astellas, and Daiichi Sankyo. Revenue figures collected from Avention on 7/10/2015. R&D figures from Evaluate Ltd. Cash and equivalents figures collected from their respective 2014 annual reports.

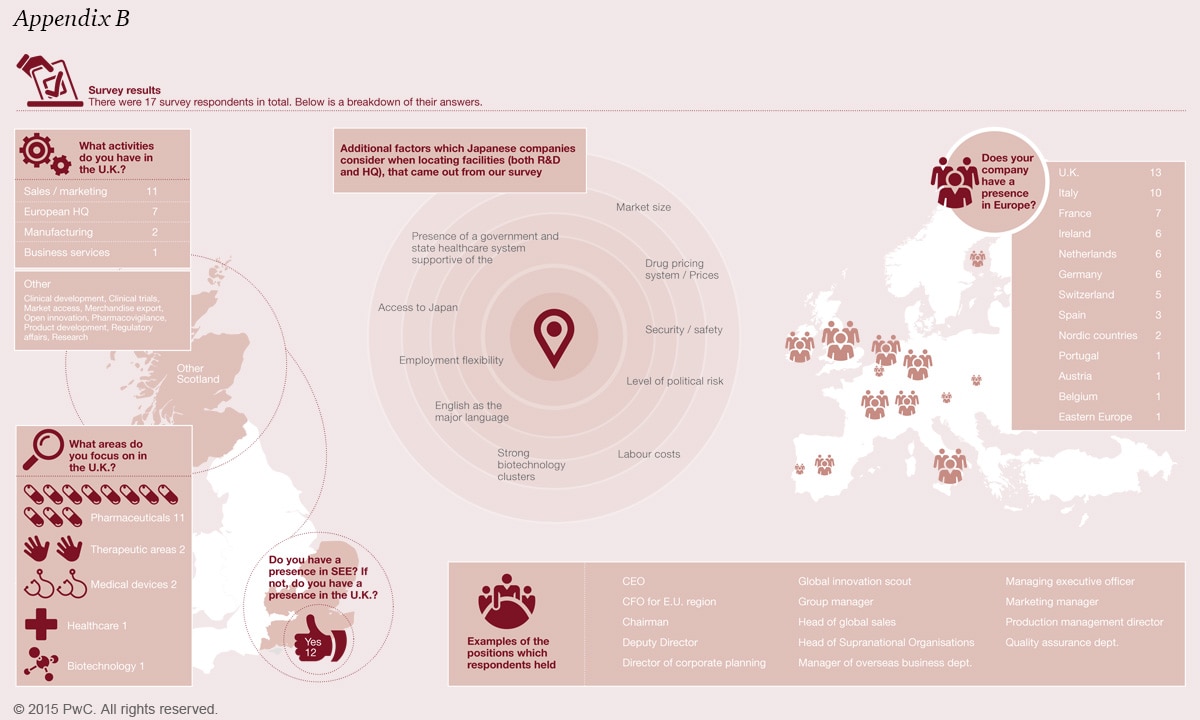

In order to complete our assessment, we conducted 10 interviews with Japanese life sciences companies. Interviews were carried out by PwC Strategy& (U.K.) in London and consultants from PwC Japan, which allowed us to reach companies both with and without a presence in South East England.

Within this group, our primary focus was on Japanese pharmaceutical companies; however, we also approached a wider range of life sciences companies that covered biotech and medical technology providers. Finally, we explored a broad range of potential investment activities, including R&D, sales & marketing, establishing a European HQ, manufacturing, and other business services.

We have consulted with seven of the 12 top Japanese pharma companies by 2014 revenue; six already had a presence in the SEE region. Survey respondents’ roles included CEO, CFO, and senior managers. Our interviews covered 61% of the R&D spend of the top 12 Japanese companies.

To be able to quantify our findings, we also released an online survey which was completed by 17 Japanese life sciences companies. The survey was designed to assess the extent of their presence in the region, their experience of operating in the South East across a set of dimensions, and key things considered when setting up in a new location.

Download PDF - {{item.damSize}}