For insurers, climate change presents the single biggest risk - and opportunity - in the coming decades. Insurers need to understand how three main categories of climate risk - physical, transition and litigation risks - will affect them and they must respond appropriately or else their financial viability may be endangered. But the message is not all negative, say Gulbahar Tezel and Mukund Rajan of Strategy&: "If you are in the business of risk, these are exciting times. There are real opportunities for insures that position themselves well in response to a decarbonizing world." A new Strategy& report to which both contributed, 'Maximising Impact', describes the actions insurers can take to thrive in the face of climate change.

To address climate change, policy makers are setting ambitious decarbonization goals and designing incentive schemes. These initiatives are reshaping sectors and economies by phasing out carbon-intensive technologies in favor of greener alternatives. As a result, the demand landscape for insurance products will be reshaped impacting both the assets insured and pricing strategies for insurance products. To remain relevant in a such a decarbonizing economy and take advantage of new opportunities, we recommend insurers do three things.

Step 1 - Deep dive into the climate risks for your portfolio

To navigate the complexities of climate change, insurers must first gain a comprehensive understanding of how three categories of risks are relevant to their portfolio.

- 1Physical risks result from extreme weather events and longer-term meteorological changes. Examples include drought-induced crop failures, flood and wildfire damage to property and flights cancelled due to storms.

- 2Transition risks result mainly from how businesses and consumers change in response to decarbonization initiatives. Examples include reduced valuations of stranded energy extraction assets and business financial losses from deindustrialization.

- 3Litigation risks result from legal action taken against insures or their customers. Examples include law suits against insurance company for underwriting new oil exploration activities or against businesses for insufficient climate planning.

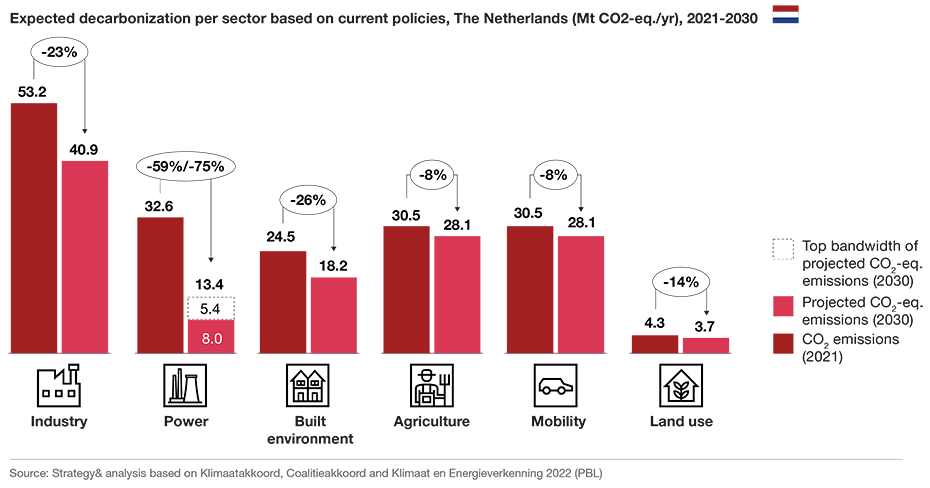

An example: expected decarbonization rates in the Netherlands

"It's key to realize that climate risks vary significantly across geographies and sectors and over time", says Tariq Abdul Muhaimin, co-author of the report, explaining why for most insurers such a deep dive will require a significant effort. "It means insurers will have to collect and process vast amounts of data, and develop a deep understanding of local climate policies." The authors of the report did exactly this in order to calculate the expected pace of decarbonization in various sectors of the Netherlands economy. Their analysis shows how emissions from the power sector are forecast to reduce by up to 75%, while agriculture and mobility emissions are expected to reduce by a modest 8% in The Netherlands.

Step 2 - Quantify the financial impact of decarbonization

The next step for insurers involves translating the insights from the deep dive into an assessment of the financial impact on their operations. This means incorporating the costs of climate risks into their technical and financial premium models, and updating risk features for each product, again taking into account sector and geography-specific considerations.

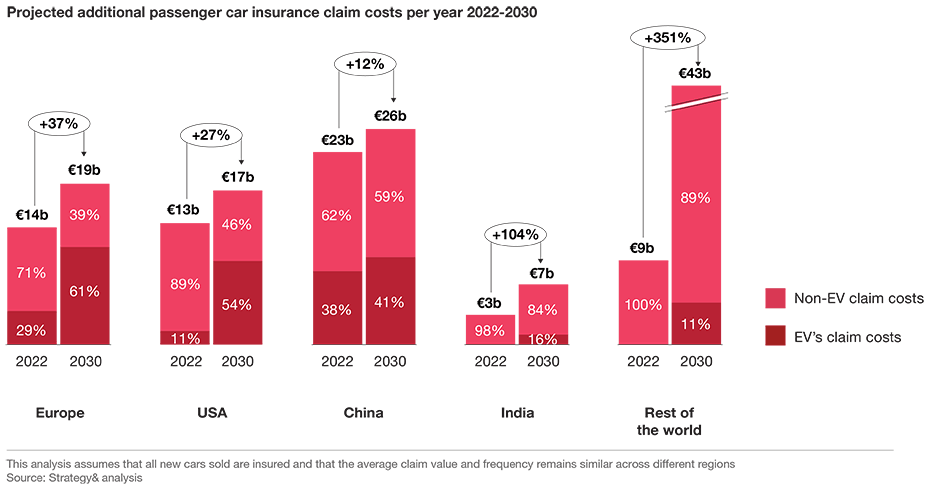

An example: expected claim costs for car insurers

For car insurers for example, decarbonization will change the composition of their portfolios as electric vehicles (EVs) will gradually replace fossil fuel cars. Since EVs have typically higher repair costs, additional fire and explosion risks and higher insured values, claim values can be expected to rise in the short term. Over time, as EV ownership becomes more affordable and widespread, this trend is likely to reverse. This ultimately translates into projected additional claim costs until 2030 as shown for a number of geographies in the exhibit below, taken from the report.

Step 3 - Evolve services offerings to respond to climate change

Based on the financial modeling done in step 2, insurers should update pricing, tighten underwriting processes and reassess the commercial viability for existing products and services. Insurers also need to develop new solutions for emerging needs, such as insurance for hydrogen pipelines or sustainable aviation fuel plants. Across all products and services, insurers need to consider their unique social obligations, and apply principles such as fair access to preventative services and affordability to climate-related insurance products. "In a decarbonizing world, insurers should thoroughly rethink what they sell, how they sell it and to whom they sell", summarizes Elizabeth Doherty, also a co-author.

Finding a new balance

To conclude, while insurers must manage new risks due to climate change, decarbonization also provides significant opportunities. By applying the approach outlined in the report, insurers can accomplish three things:

- Effectively navigate climate change complexities and play an active role in decarbonization;

- Incorporate decarbonization costs into products to maintain profitability;

- Introduce new products that meet the evolving needs of customers, adapt to the changing risk environment, and drive the transition to a sustainable future.

"For insurers to thrive in a decarbonizing world, they must find a new balance between profitability, meeting climate targets, and being seen as leading and facilitating a just and socially responsible transformation. Like we said, these are exciting times if you are in the business of risk."

Elizabeth Doherty and Tariq Abdul Muhaimin,co-authors