Physical AI: Intelligence in motion

A strategic guide to capture value as AI enters the real world

Tanjeff Schadt, and Jens Niebuhr

Executive summary

- Physical AI marks the next evolution of artificial intelligence, moving beyond digital content creation and autonomous software to AI systems that operate in the real, physical world

- The global Physical AI market is projected to reach approximately €430 billion by 2030, with significant upside potential as systems scale and mature

- Physical AI is transitioning from early pilots to scaled commercial deployment over the next 3 to 5 years. While early applications exist in constrained domains, most use cases remain in early adoption phases as technological challenges are addressed

- Value will accrue across the entire ecosystem - not only to robotics and vehicle manufacturers, but also semiconductor suppliers, cloud and data center operators, simulation and software platform providers, infrastructure players, and end users who redesign processes around embodied intelligence

- Success requires understanding where Physical AI is commercially viable today, where it remains premature, and how to position strategically across the evolving value chain

The physical AI revolution: From software into the physical economy

The defining challenge of today's AI landscape is the speed and overlap of progress. Many organizations are still translating the implications of Generative AI when the next application class is already gaining momentum. Agentic AI extends these systems by enabling autonomous planning, tool use, and execution within digital environments. Physical AI represents the next step: AI systems that operate in the real world, interacting with physical environments. These developments do not replace one another; they stack and expand the scope of AI, marking a broadening from software into the material economy and driving unprecedented AI-driven value creation.

What is Physical AI?

Physical AI refers to AI systems that perceive the physical world, reason about it, and act within it. These systems are embedded in machines - vehicles, robots, drones, medical devices, or infrastructure - and operate under real-world constraints such as physics, latency, safety, and cost. Where Generative AI focuses on producing digital artifacts and Agentic AI coordinates digital actions, Physical AI focuses on physical work: moving objects, navigating environments, manipulating tools, and interacting with humans. The defining shift is that AI becomes an autonomous actor, not just a decision-support tool, unlocking new frontiers for AI-driven value creation across industries.

What has changed is practical feasibility. Converging technologies have moved Physical AI from research ambition to commercial experimentation. Early deployments already exist across logistics, manufacturing, mobility, healthcare, and defense, with a combined Physical AI market potential of approximately €430 billion by 2030. The critical question is how companies position themselves within this emerging ecosystem to capture value across the full technology stack.

This report outlines the strategic arenas where companies can leverage their capabilities to build sustainable competitive advantage and create winning propositions in the Physical AI market.

Physical AI unlocks value first where automation pressure is highest

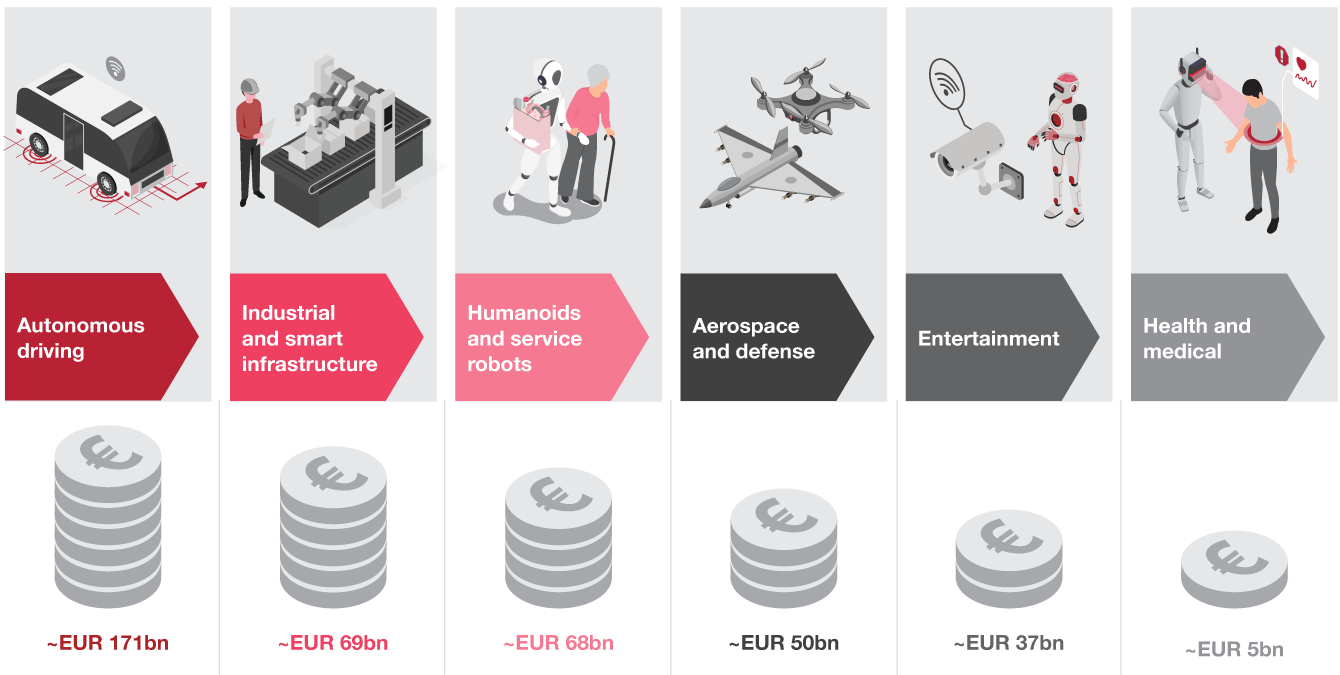

Physical AI adoption accelerates in contexts where automation delivers high economic value, environments are partially structured, and human labor is scarce, expensive, or exposed to risk. The market opportunity spans six key verticals:

Core capabilities of physical AI are advancing rapidly

Physical AI systems are built on three tightly integrated capabilities: sensing, decision-making, and actuation:

Advances in multimodal sensor fusion and perception are improving how Physical AI systems estimate their own state and understand their environment in real-world conditions. Progress in planning, reasoning, and input integration enables robots to choose and sequence actions even in uncertain or noisy environments. Meanwhile, improved actuators and control systems are increasing precision, energy efficiency, and responsiveness, allowing safe operations at higher speeds.

These capabilities operate under strict constraints on energy, safety, and system reliability, placing new demands on underlying infrastructure and driving AI-driven value creation across the technology stack.

The embodiment gap shapes market adoption patterns

Despite rapid progress, Physical AI still lags humans performance in adaptability to highly unstructured environments, manipulation of diverse objects, and context-aware human interaction. These embodiment gaps reduce reliability and versatility outside controlled settings.

However, Physical AI now exceeds human performance in constrained tasks requiring high precision, repetition, advanced sensing, and rapid control loops. These asymmetries explain why early commercial success is concentrated in logistics, manufacturing, and mobility rather than general robotics.

As Physical AI systems transition from research to scaled deployment, value creation increasingly shifts from standalone hardware toward compute, foundational software, and system integration - reshaping markets and value pools across the ecosystem.

Physical AI adoption and value distribution

Physical AI adoption will be concentrated in high-value sectors, with the automotive sector leading at approximately €171 billion of the €430 billion global Physical AI systems market by 2030, followed by industrial automation and warehousing at €69 billion. For Europe, early adoption will represent approximately €80 - 110 billion by 2030.

Three key value concentration areas along the technology stack:

- Digital infrastructure – High-performance compute and memory create bottlenecks that concentrate value among leading chip suppliers

- Foundational models – Multimodal AI "brains" that perceive, plan, and act autonomously capture large shares of software value

- Simulation platforms and world models – Enable virtual training and testing before deployment, reducing cost and risk

For companies aiming to capture a significant share of the value potential of Physical AI, it is imperative to make conscious decisions on where and how to play in this highly competitive and fast-changing industry.

Strategic arenas shaping competitive advantage in the Physical AI ecosystem

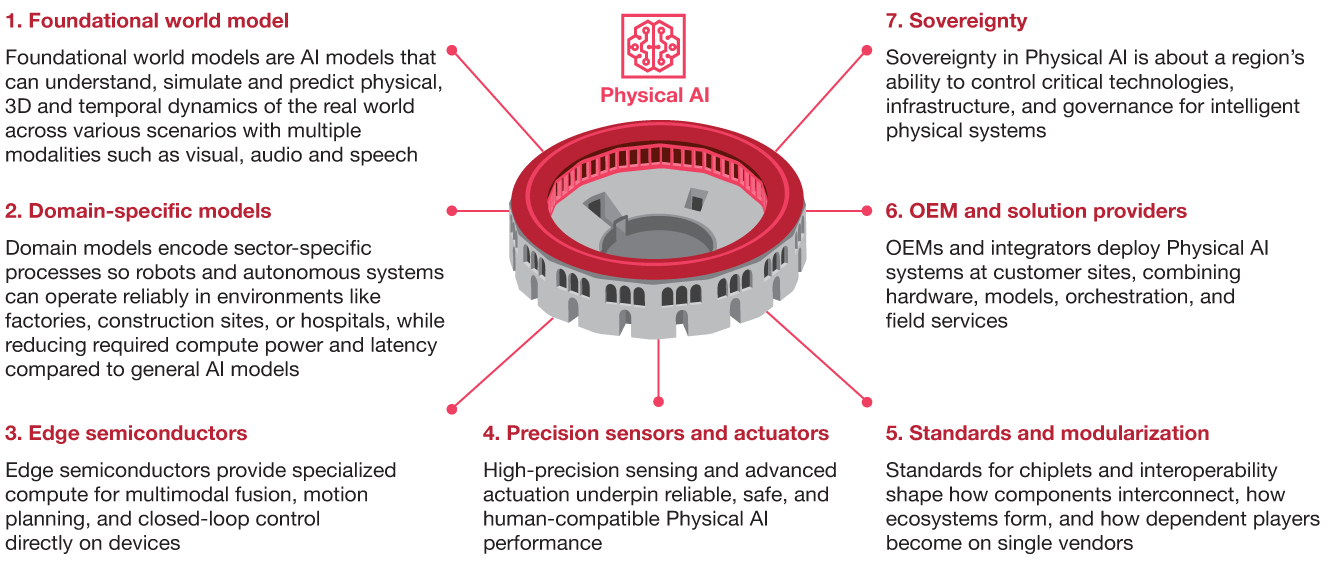

Building on these value pools, the Physical AI era is taking shape around seven key arenas that govern how intelligent machines are built, deployed, and controlled. Each arena presents distinct value creation strategies, control points, and risks for both global leaders and European companies seeking to balance competitiveness with strategic independence.

Intelligence is moving beyond the screen

For the first time, AI systems can perceive, decide, and act in the physical world as autonomous agents reshaping how physical work gets done. This changes the strategic calculus: while digital AI disrupted information work, Physical AI will disrupt physical operations. The companies that control how machines understand and interact with the physical world will hold structural advantages for decades.

The window to shape this landscape is narrow

Foundational models, simulation platforms, and semiconductor architectures are being defined now. Data flywheels are spinning up, and standards are forming. Within 3 - 5 years, the first generation of Physical AI leaders will be established, and the cost of catching up will be prohibitive. Strategic decisions on platform partners, data strategy, and in-house capabilities must be made within the next 12 - 24 months.

Three questions require immediate executive attention:

- Where will you compete - and where will you depend?

- What proprietary assets can you build before the window closes?

- How do you move fast while keeping strategic optionality?

Andy Ogrins, Martin Gerhardus, Stanislav Huley, Dr. Richard Weller, Andrea Deublein, Cedric Rohm, and Matthias Brecht have contributed to this report.