How Europe can embrace the generative AI opportunity

Seizing the vast potential of GenAI

Dr. Philipp Wackerbeck and Dr. Matthias Schlemmer

A decade of generative AI

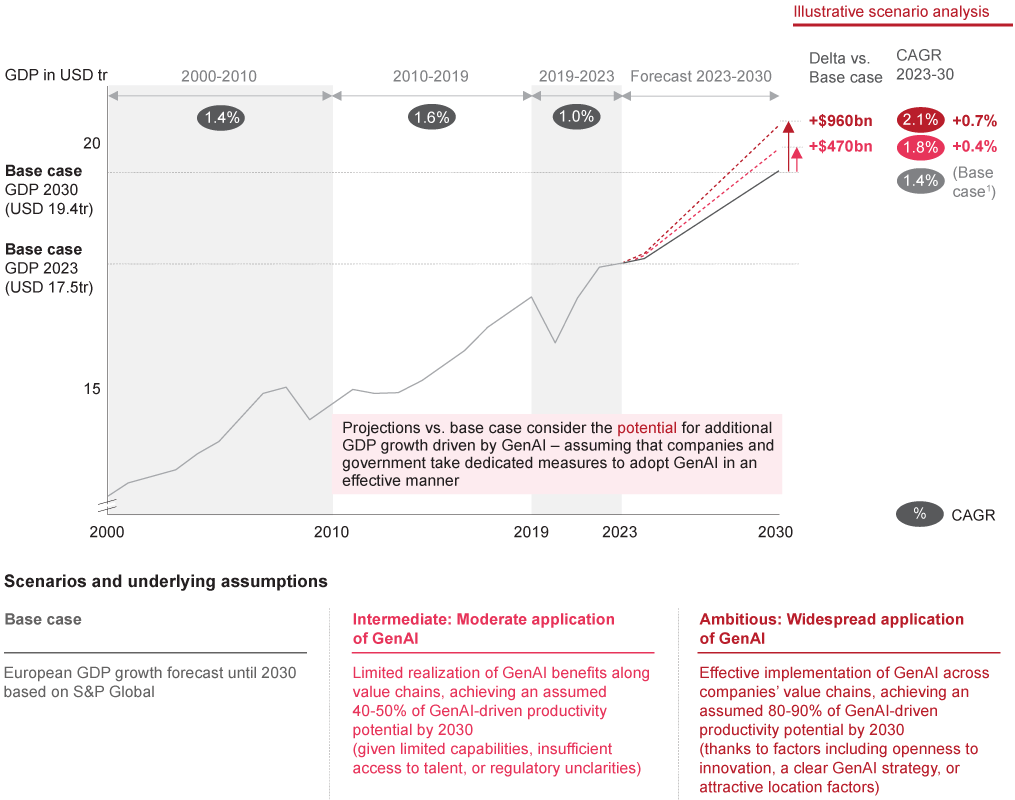

Generative artificial intelligence (GenAI) is considered one of the most important technologies of our time, and the next ten years will be shaped by advancements driven by GenAI. The potential impact is significant: it could potentially boost Europe's annual GDP growth by 0.4% to 0.7% by 2030, a substantial increase compared to the forecasted growth rate of around 1.4% without AI effects. This technology has the potential to address Europe's ongoing shortage of skilled workers and provide companies with competitive advantages in both the short and long term if they quickly adopt generative AI.

This report explores the impact of technology on businesses and economies in Europe in the coming years. It examines which industries and countries will be most affected by the opportunities and challenges of generative AI, and discusses strategies and public policies that can support the growth of GenAI capabilities in business.

What is generative AI?

GenAI represents a significant advancement in terms of variety, flexibility, and ease of use. It is capable of responding to queries that a non-expert person might pose, producing outputs that incorporate visuals, audio, and text in multiple languages. This automated intelligence system is more sophisticated than any previous automated intelligence and learning application, yet simpler in terms of usability.

Potential by industry

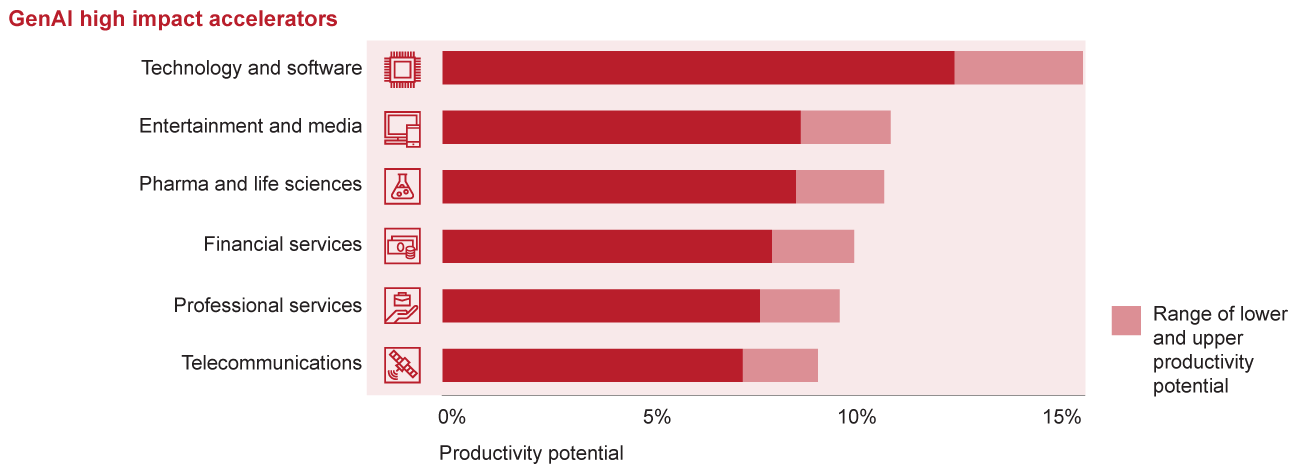

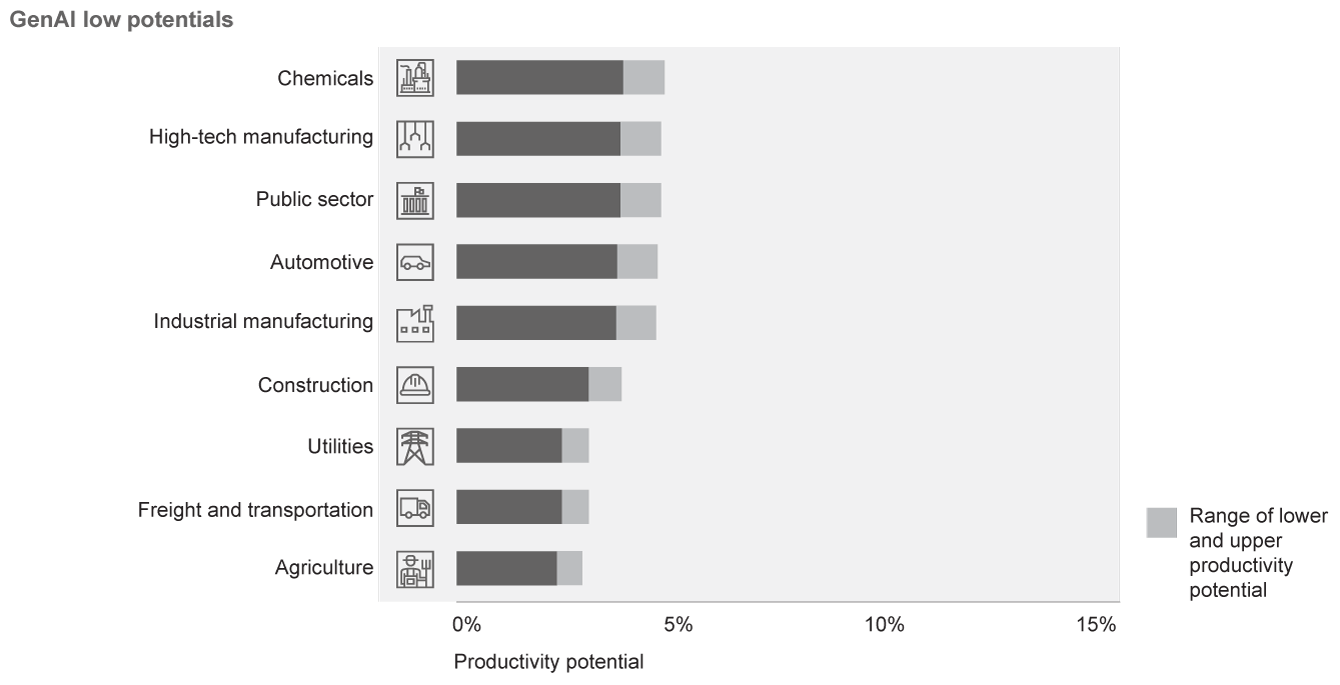

The potential benefits of generative AI are unevenly distributed across sectors. Therefore, implementation of the technology will tend to increase the value-added differential between different industries. Across sectors, companies can maximize the advantages of generative AI through careful assessment of internal use cases, seen through the lens of real-world productivity gains. The technology’s potential for different industries can be defined as:

Companies that have the potential to accelerate the development of the GenAI family of technologies and achieve rapid impact both on revenues and bottom-line performance.

Companies that can capture new efficiencies from GenAI applications developed largely outside their own domain, with impact on the bottom line.

Physical labor or production dominates the value chain and automation, supplemented in part by GenAI, can make a notable but lower contribution to productivity.

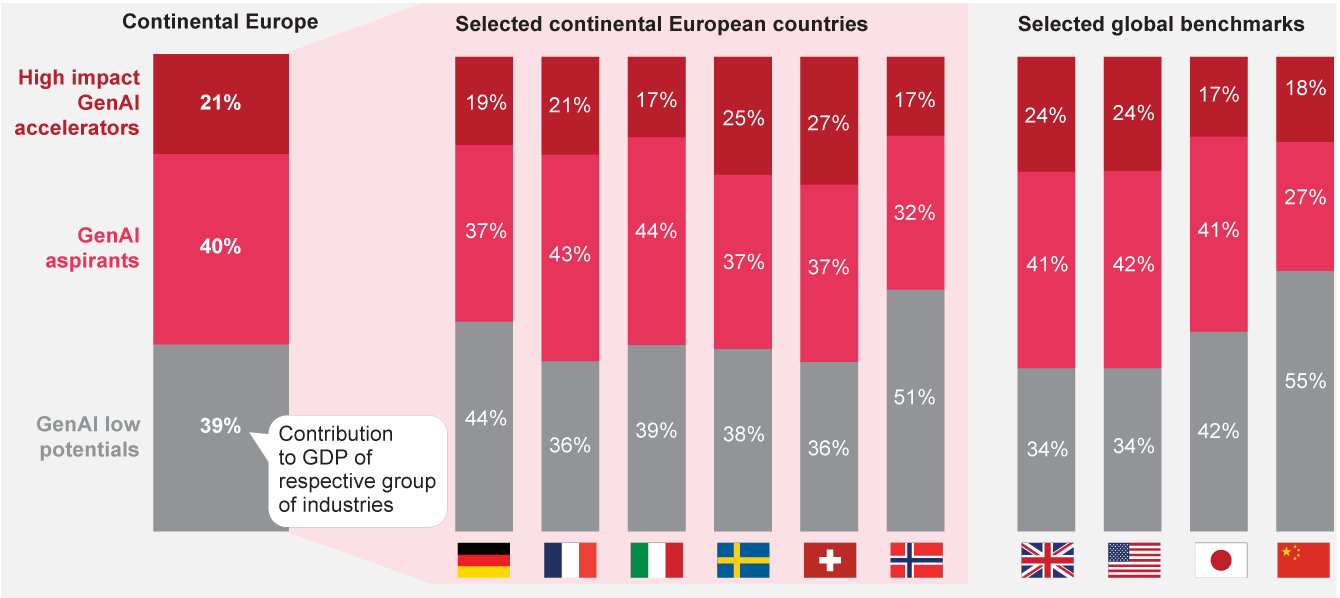

Advantage by country

Countries that rely heavily on industries such as technology, entertainment, life sciences, financial and professional services, and ICT are poised to see significant boosts in productivity and revenue by effectively integrating generative AI into their operations. Meanwhile, countries where industries like agriculture, utilities, construction, manufacturing, retail, and support services are more prominent can also experience benefits from adopting this technology, although the impact may not be as transformational.

GenAI potential on continental Europe’s GDP

Our research indicates that implementing generative AI in European countries could potentially increase GDP growth by 0.4% to 0.7% by 2030. This could result in an additional $1 trillion in GDP by 2030 - a massive boost to GDP in an era of historically low economic growth, which is currently forecast to be below 1.5% between now and 2030.

We have derived two implementation scenarios to map the effects of GenAI, in addition to a ‘no-change’ base scenario:

Under this best-case scenario, Europe will see high-impact accelerator businesses take an increasing share of the economy, and 80% to 90% of potential GenAI-driven productivity gains will be achieved by 2030. Total impact: an additional 0.7% GDP growth

Under this moderate-case scenario, Europe has only limited success in attracting or developing more high-impact accelerator businesses, and no more than 40% to 50% of potential productivity gains are realized by 2030. Total impact: an additional 0.4% GDP growth

Ten success factors for a smooth and effective generative AI transition

To capture maximum benefit from the GenAI decade, there is an urgent need for European companies and governments to review and extend their strategy and policy approaches in the following key dimensions:

Martin B. Rietzel has co-authored this report.