Nearshoring vs. offshoring

Why CEOs must move beyond best-cost-country thinking to unlock full potential of value chain configuration

Michael Weiss and Thomas Ketterle

Executive summary

- European manufacturers re-shore billions in economic value to cut costs, generate growth, and increase time-to-market, predominantly to Central and Eastern Europe rather than Asia

- CEE nearshoring business cases for manufacturing struggle in today's reality (further intensified through US tariffs), and often fail to deliver the expected savings and contribution to competitiveness

- Offshoring production to Asia delivers 55% labor arbitrage versus Central and Eastern Europe, while China's automation density exceeds European levels by 2-6x

- No single location archetype holds a universal advantage. The decisive question is no longer where to cut costs, but how to configure the production footprint to drive both performance improvement and revenue growth

- A comprehensive approach is needed to evaluate strategic responses to global competition beyond basic costs and combine nearshoring with internal restructuring, offshoring, automation and local market upsides

Why nearshoring strategies require reassessment

European manufacturers face mounting pressures with no relief in sight for 2026. Across the continent, companies consistently rank competitiveness concerns among their most severe risks, with over 25% expecting business conditions to deteriorate and nearly 80% struggling to predict the future amid geopolitical and economic uncertainty.

Yet the strategic playbooks most companies rely on were written for a different era – one where production nearshoring meant speed, offshoring meant cheap, and domestic meant quality. Those stereotypes have expired: No single location archetype holds a universal advantage anymore. Speed to market is now achievable in Asia. Advanced automation and strategic supplier partnerships can make domestic production competitive. Meanwhile, markets once considered low-cost havens face rising wages and skilled labor shortages.

Our study evaluates how value chain configuration must evolve, analyzing four forces reshaping manufacturing competitiveness:

- persistent structural pressures including energy and labor costs,

- shifting investment flows away from Europe,

- Asian overcapacity and export pressures, as well as

- advances in AI-driven manufacturing and robotics.

Our conclusion: The question is no longer nearshoring versus offshoring. The decisive question is how to configure your current production footprint to drive both operational performance and revenue growth. Companies can achieve this only by moving beyond fragmented, cost-driven relocation decisions and combining nearshoring with internal restructuring, selective offshoring, and automation investments. The strategic imperative is unlocking the full potential of value chain configuration - not just for margin improvement, but for competitive differentiation and market agility.

"CEOs can no longer rely on location as a competitive lever. The question isn't where to produce – it is how to configure your entire value chain to unlock both efficiency and growth. That requires moving beyond outdated stereotypes and fragmented cost decisions."

Michael Weiss

Partner, Strategy&

Performance and Restructuring Lead

Competitiveness doom loop

Firms are increasingly trapped in vicious cycles where stagnant productivity, organizational complexity, and fragmented location decisions erode competitiveness:

Weak economy and margin pressure → Erosion of competitiveness → Short-term cost actions (nearshoring, layoffs) → Tech/automation initiatives that frequently underdeliver → Limited productivity gains due to organizational complexity → repeat.

-

Weak economy and margin pressure

Firms face cost sensitivity and pressure to maintain market position

-

Erosion of competitiveness

Reduced pricing power and high costs vs. global peers weaken competitive position

-

Short-term cost actions

Nearshoring and layoffs improve cost positioning but do not address underlying productivity gaps

-

Tech/automation initiatives

Invest in digitalization, AI and automation frequently underdelivers in practice (e.g., due to skill gaps)

-

Limited productivity gains

Organizational limitations (e.g., org. complexity) prevent benefit scaling

Legacy playbooks from an era of growth and limited competition have become liabilities. C-suites have expanded by 160% from 1990 to 2023, concentrating decision-making at headquarters and often slowing adaptation to rapidly changing market environments – precisely when speed of reconfiguration has become a competitive differentiator.

The nearshoring paradox: Germany deep dive

Many German manufacturers might find themselves in a competitiveness doom loop. Rising labor costs and weak productivity growth are eroding the country's cost competitiveness at an alarming rate. German labor costs now stand approximately 30% above the EU average, compressing manufacturing margins and forcing difficult strategic decisions.

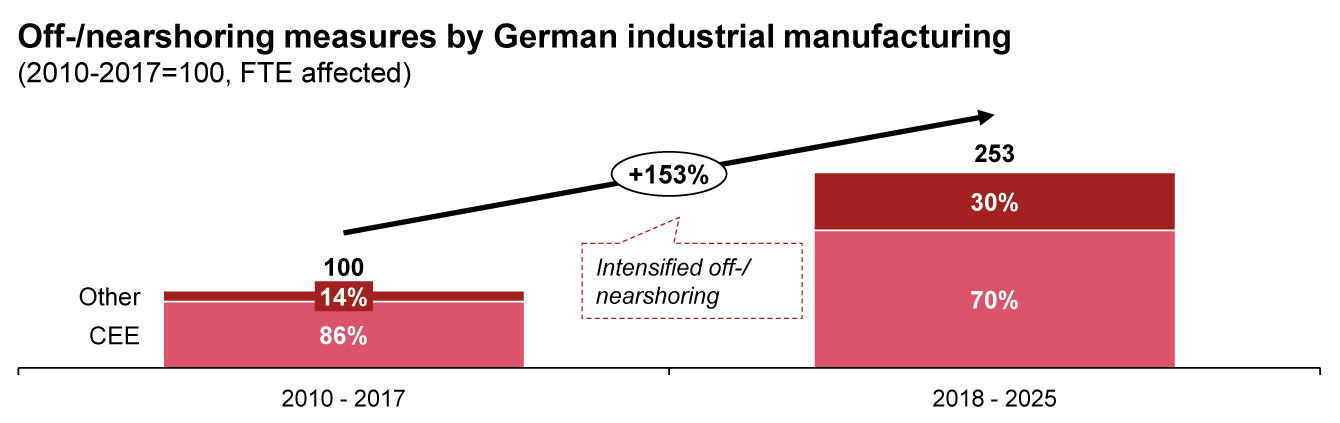

External shocks – Covid-19, the war in Ukraine, and the energy crisis – have amplified these pressures, accelerating a trend that was already underway. In response, German firms have increased off- and nearshoring activities by 153% between 2018-2025 compared to 2010-2017, with 70% of relocated operations moving to Central and Eastern Europe (CEE).

The evidence suggests it is time for a critical review. Many nearshoring initiatives have failed to deliver expected savings. Simple lift-and-shift relocations no longer bring relevant competitive advantages. Companies making fragmented, risk-averse decisions for individual sub-functions find that original advantages have become marginalized, increasingly tying up headquarters management capacity without delivering differentiation. Markets that once appeared attractive have not always developed as expected - costs have risen, skilled labor has become scarce, eroding the arbitrage that justified the move. Moreover, focusing solely on costs prevents companies from realizing growth potential available through strategic value chain reconfiguration.

Nearshoring and offshoring considerations

Production relocation decisions should be driven by quantified cost and value tradeoffs – not "comfort-driven" proximity or outdated assumptions about speed and capability. Historical distinctions have blurred: rapid time to market is now achievable in offshore locations, while automation and supplier partnerships can make domestic production competitive. Domestic cost pressure, automation and optimization, market proximity, and strategic importance are key when considering nearshoring or offshoring.

Common pitfalls hindering right-shoring:

-

Gut-feel decision-making

Gut-feel decision-makingCompanies often react to a “feeling” that costs are high or follow peer behavior, without quantifying the actual cost gap (domestic vs. nearshore vs. offshore)

-

Nearshoring by default

Nearshoring by defaultNearshoring is often chosen by default, but investment in automation and optimization (e.g., processes) may be more efficient, especially as nearshoring locations become less cost advantaged

-

Misaligned drivers

Misaligned driversNearshoring should be driven by value derived from proximity to customers or other operations (shorter lead times, flexible response), not just fear of offshoring

-

Non-strategic relocations

Non-strategic relocationsCompanies often nearshore operations that are not part of the core capabilities and do not hold strategic importance, out of convenience

Time to rethink nearshoring

To stay competitive, turn shoring decisions into direct P&L impacts, and unlock new growth, the following questions need to be addressed:

- 1Performance improvement: What measurable profit and loss impact has your nearshoring strategy delivered in the past 12 months?

Are you capturing margin improvement and top-line growth through differentiation, or only pursuing labor cost reduction? - 2Automation: Is your automation strategy genuinely reducing dependency on location arbitrage and creating opportunities for competitive domestic production?

- 3Disruptive developments: Does your planning account for emerging megatrends like physical AI and their potential impact?

- 4Nearshoring: Is nearshoring still a competitive advantage, or has it become an inherited assumption no one is challenging?

Have the original advantages become marginalized while management capacity is increasingly consumed? - 5Offshoring: Does your current production footprint enable global cost competitiveness and resilience?

Or are you making fragmented decisions that miss the best possible configuration among all available options?

Michael Meyer co-authored this report.

Nearshoring vs. offshoring

Contact us

Michael Weiss

Partner, Performance & Restructuring, Strategy& Germany

Thomas Ketterle

Partner, PwC Germany