Key Takeaways

- "Golden Twenties" of transformation in Financial Services: Driven by the compounding risks of outdated legacy systems, the retirement of mainframe experts, and compulsory DORA compliance, core system transformation is now an existential imperative.

- Widening structural divergence: While major private banks and P&C insurers have been the first to pivot to modular, AI-ready cores, cooperative and savings banks along with life insurers have kept longer with legacy mainframes.

- Trading the "big bang" for phased agility: Successful transformations are abandoning "big bang" replacements in favor of a nuanced "phase it to ace it" approach, deconstructing the core, simplifying product portfolios, and leveraging agentic AI to increase efficiency.

Change imperative in Financial Services

The financial services industry is currently navigating a period of technological metamorphosis in its backbone fundamentals. For many years, the prevailing strategy was to "freeze the core," wrapping established mainframe systems into middleware configurations to enable digital front ends without disturbing the underlying ledger. However, we have entered what we call the "Golden Twenties of Change," a period where core modernization has shifted from IT aspiration to strategic necessity.

This shift is not driven by one factor in isolation. Increasing reliance on a narrow ecosystem of third-party specialists, accumulating technical debt, and the approaching "skills cliff" with the retirement of mainframe experts, all contribute to a significant operational risk. Simultaneously, regulatory frameworks such as DORA enforce stricter standards for operational resilience - standards that opaque legacy architectures in some cases struggle to meet. Furthermore, many large-scale transformations have historically been pushed back, as their timelines often exceed the typical tenure of C-Suite executives. This has resulted in a significant market backlog. Consequently, the boardroom conversations have moved away from when to start transformation and toward how to plan and deliver complex programs effectively.

To understand how organizations are navigating this shift, we conducted an analysis of the German banking and insurance landscape. Our insights are grounded in research evaluating over 1,800 banking and insurance institutions, alongside direct interviews and quantitative surveys with selected executives from renowned banks and insurance companies.

The state of the industry: A structural divergence

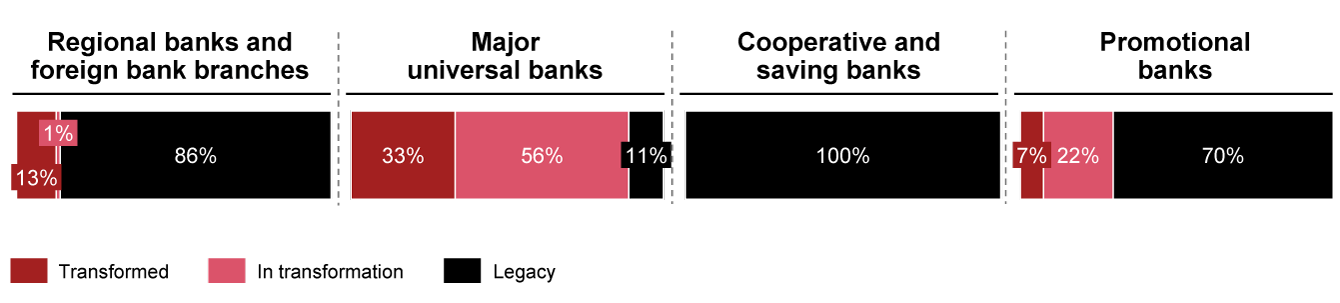

Our latest analysis of the German banking and insurance landscape reveals that progress in transformation is not uniform; rather, it is defined by a structural divergence based on legacy dependencies and architectural complexity.

In the banking sector, major private banks are leading the transition. Approximately 56% of these institutions are either fully transformed or actively modernizing, driven by the need to decouple retail operations from global investment banking architectures and compete with agile market entrants. By contrast, the cooperative and savings bank sectors show a different trajectory, with 100% relying on established legacy platforms. For these institutions, centralized mainframes (such as OSPlus or agree21) continue to process high transaction volumes at low unit costs, often making the business case for a full cloud-native replacement challenging in the absence of a compelling catalyst.

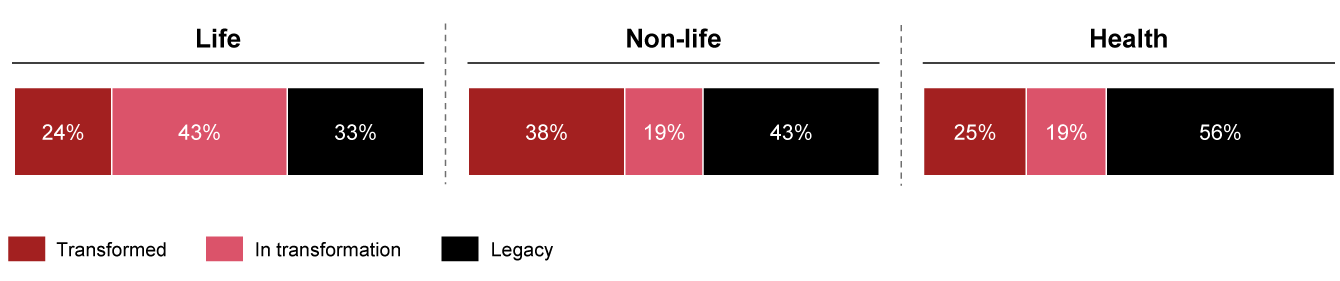

In the insurance sector, structural divergence is driven by product complexity. Non-life is leading the way, with 38% transformed insurers and 19% in transformation, forced into API-enabled ecosystem connectivity by pricing aggregators and annual policy renewals. On the other hand, 43% of life carriers have initiated modernization but lag significantly behind in transformation completion (24%), as they operate with long-term product horizons. They must replicate decades of different and complex financial guarantees under strict regulation, meaning that historical margins and solvency requirements encourage them to incrementally patch legacy mainframes and to delay complex migrations. Lastly, deeply localized German requirements like statutory aging reserves anchor 58% of health insurance players into legacy.

Evolving vendor strategies

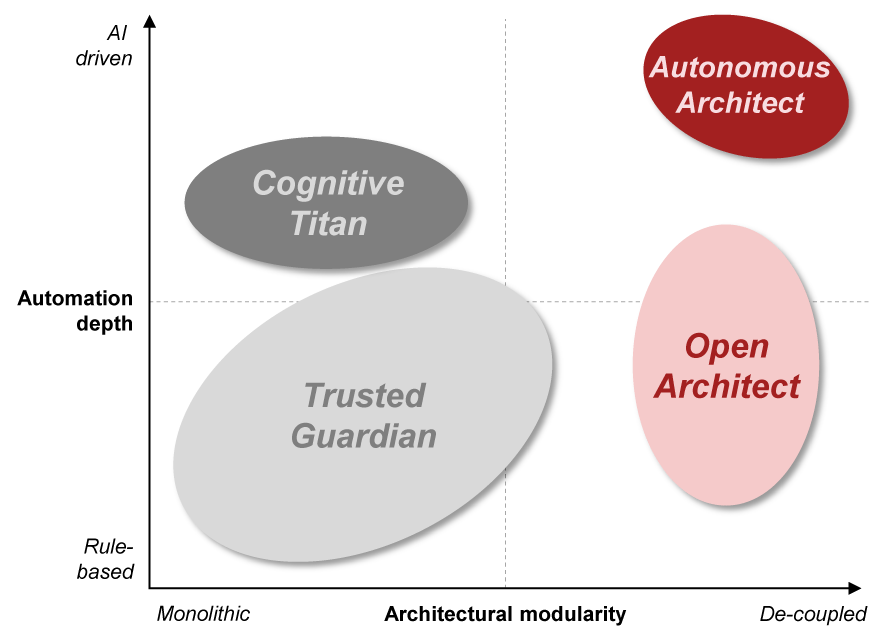

As the market matures, the era of the generic "core banking system" has ended. Vendors are no longer competing solely on product feature lists but are aligning themselves with specific strategic archetypes that mirror the evaluation in the industry along the dimensions of “automation depth” and “architectural modularity”. Hence, core system suites fall into four distinct archetypes, as shown in the following exhibit:

In the banking sector, the vendor landscape appears to be segmented based on the trade-off between architectural autonomy and operational stability.

- Increasingly, private banks seem to be evaluating "Cognitive Titan" and "Autonomous Architect" platforms. These solutions position the core system as a programmable asset, leveraging cloud-native infrastructure to establish the consistent "single source of truth" essential for deploying high-performance AI capabilities.

- In contrast, the cooperative and savings sector is leaning toward "Trusted Guardian" models. These monolithic platforms emphasize today’s compliance and stability, providing standardized “all-in-one” solutions for core operations, rather than orchestrating third-party components.

- Complementing these archetypes, the "Open Architect" is mainly tailored for regional players and foreign bank branches. Operating as a cloud-native hub, these platforms utilize standardized APIs to bypass legacy limitations and enable the seamless integration of specialized third-party fintech models.

In the insurance sector, core system suite vendor strategies seem to be fundamentally shaped by the specific nature of the underlying risk portfolios.

- Life insurers, along with large health carriers, appear to be leaning toward the "Trusted Guardian" archetype. These comprehensive platforms centralize the entire policy and claim lifecycle into a pre-integrated suite, offering an integrated approach to managing regulatory safety, data integrity, and actuarial precision.

- By contrast, non-life carriers increasingly seem to leverage the "Open Architect" model. Favoring a modular approach, these API-first infrastructures are orchestrated via the cloud and engineered for speed-to-market, enabling rapid product-as-code configuration and instant component swapping.

- Transcending these vertical splits is the "Autonomous Architect". Rather than completely replacing the primary core, this archetype focuses on decision efficiency by acting as an intelligent overlay, deploying AI agents to handle unstructured data and augment high-friction workflows like claims and underwriting.

- Additionally, large-scale insurers seeking out-of-the-box intelligent automation without decoupling their architecture seem to be targeting the "Cognitive Titan", which embeds advanced AI natively into a unified, monolithic system.

A strategic blueprint for core transformation

Navigating this complex landscape requires more than just technical upgrades; it demands a holistic approach to transformation. Our research highlights that successful organizations integrate 5 strategic levers to de-risk their journey and maximize value.

- 1To mitigate the operational paralysis often associated with "big bang" replacements, CIOs are prioritizing flexibility for stability, designing a transformation architecture that allows for long-term parallel operations. This approach focuses on reducing the architectural complexity of the legacy core by initially removing add-on functionalities. Subsequently, functionalities are gradually built into the target system running in parallel, for step-by-step migration.

- 2However, architectural agility must be preceded by portfolio rigor. A critical enabler is the strategic decision “simplify to amplify”, rigorously streamlining the product portfolio to prevent the migration of legacy complexity. By identifying and discontinuing products with high maintenance costs but low transaction volumes and modularization of product features, banks can prevent the costly effort of re-platforming legacy debt, thus ensuring that resources and operations are focused on value creation and ready for transformation.

- 3This level of prioritization requires organizations to unify to magnify their resources, reframing transformation as a joint venture where business and IT manage decisions together. When business capabilities drive decisions, e.g., "speed vs. stability" or "build vs. buy", institutions avoid the watermelon effect (looking green outside but red inside) and ensure investments target true competitive differentiators.

- 4When moving from strategy to execution, the industry has pivoted to a "phase it to ace it" roadmap, replacing high-risk cliff-edge cutovers with a calibrated, de-risked sequence. This path (rationalizing the legacy core, preserving data integrity through parallel "shadow" processing, and only scaling new features once the foundation is secure) allows for incremental validation and significantly reduces the blast radius of potential operational issues.

- 5Finally, the defining differentiator of the "Golden Twenties" is the capacity to use AI to multiply efficiency across the value chain, evolving Artificial Intelligence from a peripheral tool into a core accelerator. In the migration phase, agentic AI is now deployed to analyze millions of lines of legacy code and to document lost business logic; in the target state, it transitions to operational roles from automated verification to predictive liquidity management, collapsing traditional build barriers and enabling institutions to scale proprietary capabilities at unprecedented speed.

In conclusion, the "Golden Twenties" represent a unique window of opportunity. As technological debt and the competitive landscape shift, the cost of inaction is rising. However, the path to a modern core is no longer a leap of faith. By aligning with the right vendor strategy and adopting a disciplined, phased, and business-led approach, financial institutions can transition from maintaining legacy liabilities to orchestrating intelligent, future-ready ecosystems.

The dawn of the next-decade financial services player

The "Golden Twenties of Change” in core system transformation lay the ground for highly automated financial services ecosystem players. As banks and insurers decouple legacy architectures, the industry focus will shift from basic infrastructure replacement toward vastly accelerating the delivery of core business operations. Banking in 2035 will still revolve around accounts, cards, and payments, just as the insurance sector will continue to center on policies, premiums, and claims. The focus of future differentiation does not lie in replacing these bedrock products, but in how the customer interaction and transaction processing are delivered intelligently and without frictions:

- The evolution of agentic AI: Moving beyond its current role as a legacy migration tool, agentic AI will mature into the central nervous system of the enterprise. AI ecosystem collaboration will autonomously orchestrate complex operations and customer interaction along the product lifecycle, driving zero-touch claims processing, dynamic credit decisioning, next-generation product sign-up, and real-time liquidity management.

- Symbiosis of strategy and vendor ecosystems: The financial services technology landscape will move beyond binary architectures, into an interdependent ecosystem. Banking and insurance players will blend composable API-first, AI-enabled vendor platforms to deliver innovation, resilience, security and compliance, and scale to their customers.

- From static ledgers to a dynamic ecosystem hub: The future core will evolve from a static record keeper into a highly composable architectural hub. This configurable engine will seamlessly integrate AI fabrics, blockchain smart contracts, and third-party data. Early movers will plug directly into broader partner ecosystems to deploy next-generation touchpoints like virtual branches, turning core technology into a competitive moat.

Marc Peiter, Adrian Wepner, Alen Rapo, Julian Höhler, Wieland Schlehufer and Jonathan Boße also contributed to this article.