From 2021 to 2023, the semiconductor chip shortage cost the German automotive industry in excess of €100 billion, a considerable dent in the country’s overall economic output. However, with another similar crisis on the horizon, many companies are still only ready to respond with reactive measures. What is needed is a structured and methodical risk management strategy to properly confront the long-term and systemic challenge of repeated chip shortages.

Semiconductor chips are increasingly critical to the functioning of the automotive industry. A high-end electric vehicle, for example, requires around 3,000 chips. As electric cars grow in popularity, and become even more sophisticated and complex, the demand for chips will only rise. Indeed, forecasts suggest that the automotive semiconductor market will grow several times faster than global automotive sales over the next five years, reaching a market value of $140 billion.

However, various factors threaten the smooth supply of the chips the industry so badly needs. The automotive sector has to compete with the rapidly growing tech sector that also relies on semiconductors. Moreover, international supply chains are fragile. Around 60% of the chips used in European premium cars are sourced from abroad, leaving the industry vulnerable to geopolitical tensions, such as between China and Taiwan. The concentration of essential raw materials further heightens the exposure to political crises, technical failures and logistical bottlenecks. Approximately 80% of the ultra-quartz required for chip production emanates from the United States, while 90% of gallium comes from China.

The destructive impact of shortages

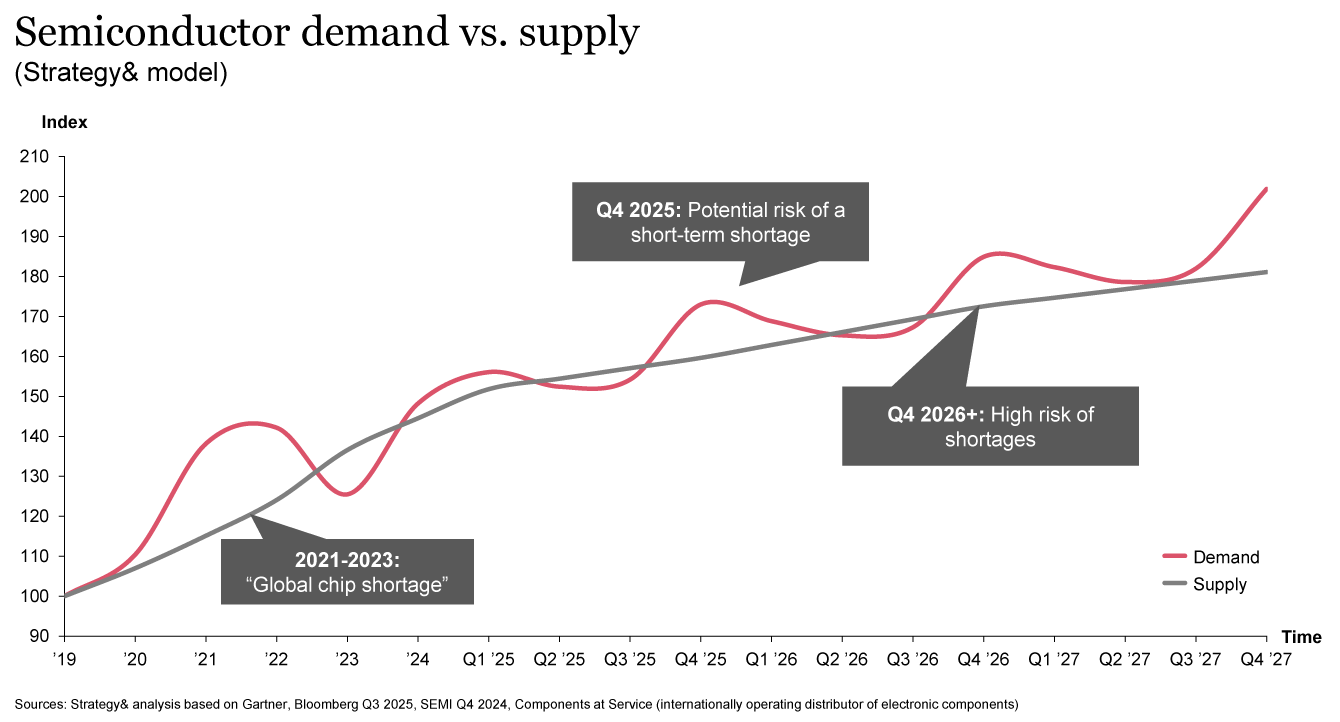

We saw the huge economic damage of semiconductor shortages between 2021 and 2023, when the German automotive industry lost more than €100 billion, equating to around 2.4% of the country’s gross domestic product. Furthermore, this figure does not even include secondary effects, such as the costs of designing chip alternatives and building inventories to secure supply. Our analysis strongly suggests that this crisis was not a one-off blip, and that a high risk of major shortages looms in 2026.

However, despite the sobering experience of the last crisis and the specter of recurrent shortages in the future, much of the industry is still trapped in a short-term, firefighting mindset. This approach represents something of a hangover from the 1990s, with its overarching focus on efficiencies and cost savings. Indeed, many manufacturers still attempt to optimize their inventory to maintain liquidity, making sudden spikes in demand extremely challenging to handle.

The industry should abandon this preference for ad-hoc responses, and instead implement systematic risk management measures, such as intelligent early warning systems, further diversification of supply chains, and cross-functional crisis teams permanently on hand to react quickly to developments on the ground.

Introducing a risk management system

To compound the issue of shortages, up to 15% of premium vehicles today contain chips that were already technically outdated or on the verge of obsolescence even before production had started.

As the redesign of alternative chips is expensive and time-consuming once a vehicle is already in mass production, a sensible, future-proof approach during the initial design stage is the most effective course of action. Companies that design key electronic components to be flexible and interchangeable from the outset, with special emergency processes and pre-approved alternative solutions already in place, can then react swiftly once a crisis hits.

Establishing strategic risk management processes needs to follow three stages:

- Sense: First, companies must always be fully aware where they currently stand in relation to supply. This assessment needs to be fully comprehensive across the entire supply chain, with access to distributor and cross-industry data guaranteed, and with real-time alerts set up should certain events transpire.

- Decide: Second, they must devise an action plan with various options and a multi-scenario supply strategy clearly defined.

- Secure: Third, they must secure market access to the products and raw materials they need by making use of alternative channels.

Executing resilient semiconductor risk management requires the right talent, high-quality data intelligence, a proactive mindset, and clear governance. It demands detailed strategic thinking and deep commitment. Given the indispensability of semiconductor supply, its success will determine the future of the German automotive industry in the global marketplace, and thus the future of the “Mobility Made in Germany” initiative as a whole.