Sustainable aviation fuel study 2023

From feedstock to flight: how to unlock the potential of sustainable aviation fuel

Dirk Niemeier

The potential of sustainable aviation fuels

Sustainable aviation fuels (SAFs) are among the most important facilitators of decarbonization in the aviation industry. However current supply is inadequate and heavy investment will be required to address growing demand and fulfil regulatory targets. With a potential future demand of about 325 million tons of SAF to achieve net zero by 2050, roughly €1,000 billion in capital expenditure will be needed simply to establish SAF refineries - offering in return attractive profits to active players given the rising supply-demand gap.

This study takes a closer look on how the market dynamics are evolving, the roadblocks that are emerging along the supply chain, how the various stakeholders are tackling and overcoming these barriers to sustainable aviation fuel supply and adoption, and the potential business models that might give rise to an optimal industry ecosystem.

Current market dynamics: supply and demand

Sustainable aviation fuel has become an important topic for the aviation industry. Offtake agreements currently account for a total of around 40 billion liters of SAF in volume worldwide until 2022, with the number of announcements soaring over the last couple of years. Increasing offtake volumes are driven both by market demand to reach environmental goals, such as the aviation industry’s target of Net Zero by 2050, and stricter regulation internationally. The ReFuel EU targets also set out a blending mandate in reference to biofuels and synthetic aviation fuels in line with the Renewable Energy Directive (currently RED III).

These mandates provide a good level of certainty around investments in the development of SAF production capacities, since non-compliance is associated with significant penalties. Yet where some countries have agreed quotas, others have not. This introduces another basis for uncertainty, related to international competition.

To establish an overview of worldwide SAF demand, we selected the International Energy Agency (IEA) Net Zero Pathway as the basis for our analysis, as in our previous study. To reach the IEA Net Zero Pathway by 2050, the following SAF quotas would be required:

| 2025 | 2030 | 2035 | 2040 | 2050 | |

|---|---|---|---|---|---|

| SAF share | 2% | 15% | 32% | 50% | 75% |

| thereof PtL | / | 2% | 7.5% | 15% | 30% |

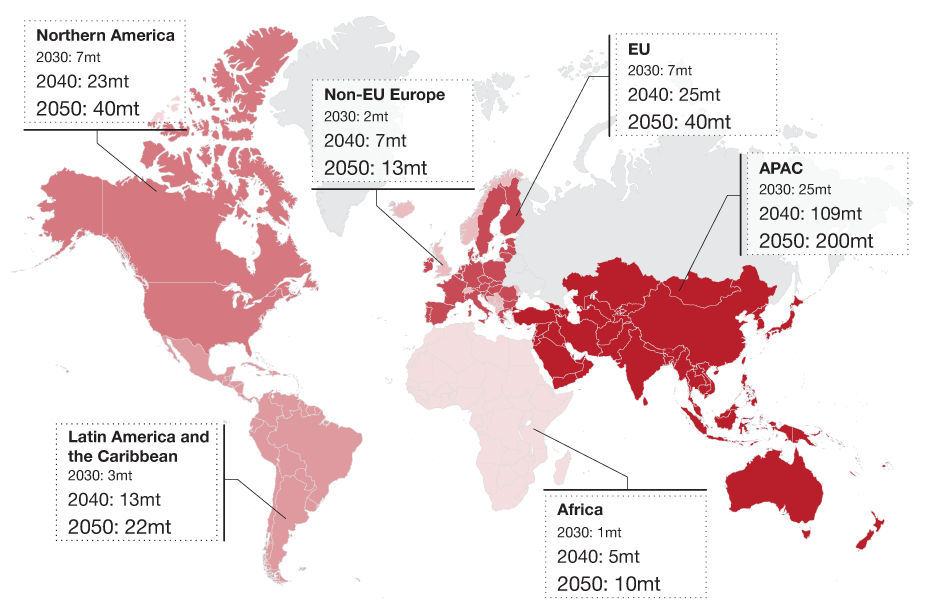

Taking into account the projected number of flights, this global SAF demand can be split across the regions. In addition to the likely regulation in APAC, the good feedstock availability, both bio-based and renewable power for green hydrogen, will give rise to enormous opportunities for this region to benefit economically from the growing sustainable aviation fuel market.

Europe’s increasingly strict sustainable fuel targets under RED III

In the EU, the 2023 revision of the Renewable Energy Directive (RED III) was adapted to account for significant changes in the transport sector, and includes strict indicative targets for more sustainable fuel use. Under RED III, the compulsory target for renewable energies in total energy consumption is now to be 42.5% by 2030, compared with 32% in RED II adopted in 2018. In addition, there is an indicative target of a further 2.5%.

The SAF value chain and its cost share distribution

A clearer understanding of where investments are needed can be gained by considering the different pathways through which sustainable aviation fuel can be produced, as each has its own relative strengths, weaknesses, and cost structures. Therefore, it is particularly important to distinguish between bio-based SAF and PtL-based SAF. While HEFA represents the most cost-efficient and mature pathway for bio-based SAF, PtL is known as the most promising future proof pathway.

The HEFA value chain

The Hydroprocessed Esters and Fatty Acids (HEFA) process represents the most mature bio-jet fuel production pathway currently. It uses vegetable oils, animal fats, waste, or residue lipids. These are treated with hydrogen to remove oxygen and break down the compounds into appropriate hydrocarbon chains, which are then isomerized (transformed to a different structure or configuration, while retaining the same chemical composition) to create SAF. With the HEFA process, it is possible to achieve emission savings of 74 to 84% compared with fossil-based jet fuel. Already certified, HEFA can be blended to a level of up to 50% with fossil kerosene without any modifications to either the aircraft or infrastructure. However, HEFA’s biological origin sets a natural cap to the available feedstock.

The PtL value chain

Power-to-Liquids (PtL)-based SAF production converts green hydrogen from electrolysis, and CO2 from sustainable carbon sources, into jet fuel and other hydrocarbon products - either via Fischer-Tropsch (FT) synthesis, or methanol synthesis. The PtL process enables CO2 emission savings of 89 to 94%. However, PtL technology is still in its early stages of development and a series of challenges exist around large-scale production.

Steps to overcome roadblocks and enable the ramp-up of sustainable aviation fuel

Across the different value chains, most of the relevant technologies for SAF production (with the exception of Direct Air Capture) are at a high level of readiness and the cost structure is understood. Yet, the supply of sustainable aviation fuel is currently insufficient. As a result, we have identified the following six main roadblocks which need to be overcome to ramp up SAF production:

- Regulatory complexity and uncertainty

- Accounting uncertainty

- High investments and market uncertainty

- Availability and scalability of sustainable feedstocks

- Scalability of SAF technology

- Low public awareness of SAF

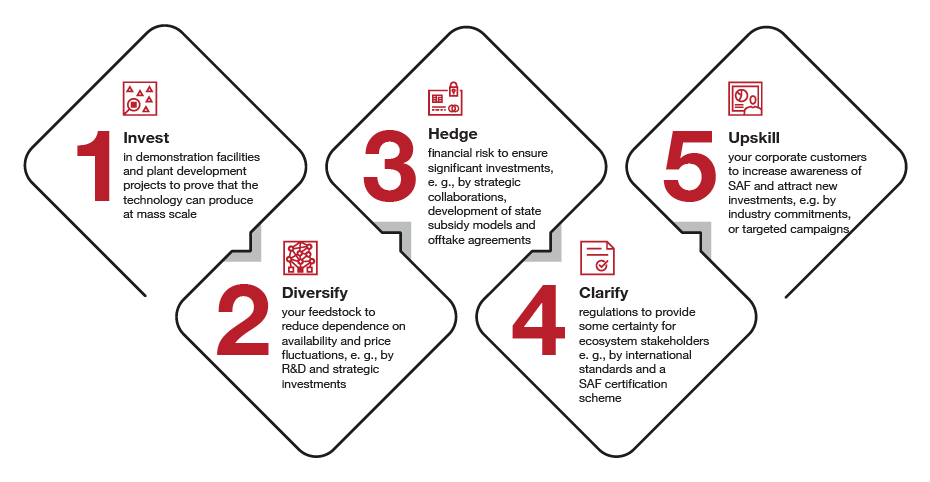

Based on this assessment of the main SAF roadblocks, we have distilled five main activities now required to provide initial stability for all ecosystem stakeholders:

Sustainable aviation fuel business archetypes

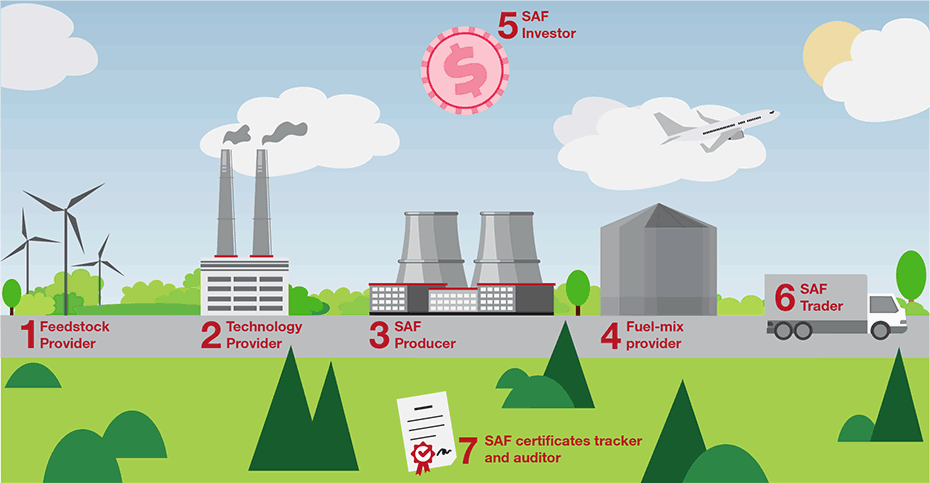

To drive the SAF market forward, all industry stakeholders will need to make a proactive and collective effort. This in turn requires the identification, establishment, and active engagement of the following sustainable and self-sustaining business archetypes:

Outlook

The scale of the task ahead, in such an international and CapEx-intense industry, cannot be solved by a single player. It requires a concerted industry effort in which each stakeholder plays its designated role while new business archetypes evolve along the SAF value chain. However, the described demand-gap is expected to sustain for the foreseeable future and thus will allow producers of SAF also to realize healthy profits when entering the market in due time. A common vision and international collaboration, underpinned by a healthy pragmatism, will be crucial to ensure that this energy transition happens – and is sustainable.

One thing is certain in all of this: climate change will not wait for human intervention to catch up. Rather, we must act collaboratively now if we are to unlock the potential of sustainable aviation fuel within an acceptable and impactful timescale.

Prof. Dr. Jürgen Peterseim, Anna Paulina Went, Florian Schäfer, Deniz Dilchert and Jonas Bruns also contributed to this report.