Steady

deposits…

2%

…outgrown

by loans

+3%

Robust

topline

1%

Stable

costs

+2%

Reduced

profit

5%

The Swiss Retail Banking Monitor is a comprehensive analysis of ~35 Swiss retail banks with balance sheet sizes above CHF 3.5bn, together accounting for over 96% of market share. Following the Swiss National Bank classification, the study includes the retail activity of large Swiss banks, Raiffeisen, regional and savings banks, cantonal banks, and selected other banks such as Migros Bank. Retail banking business data was extracted from annual reports, investor relations material and press releases. This analysis is a supplement to the larger yearly European Retail Banking Monitor.

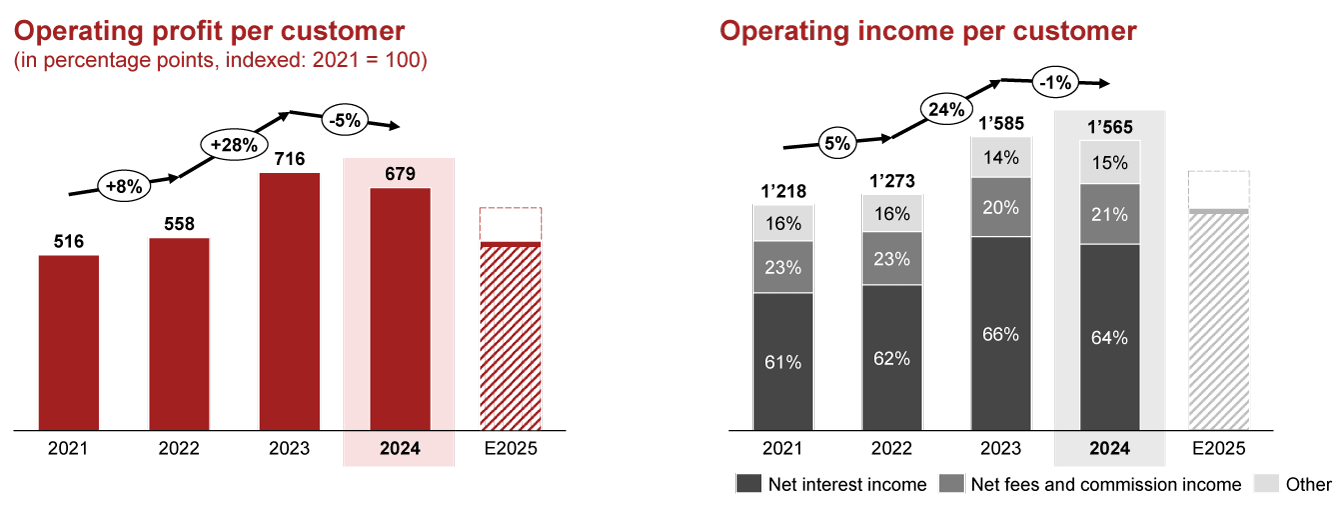

Swiss retail banks delivered record-breaking results in 2023, raising the question: Can they keep it up? 2024 proved to be another year of strong performance, marking their second-best year, with profits per customer nearly matching the previous high. It saw retail banks capitalizing on similar drivers as in the past year: A sustained interest-rate tailwind and favorable financial market developments.

However, that environment is set to change. Looking at the increasing uncertainties ahead, the development of challenger banks, and given the historically strong results of the past two years, now is an opportunity to strategically position for the years to come.

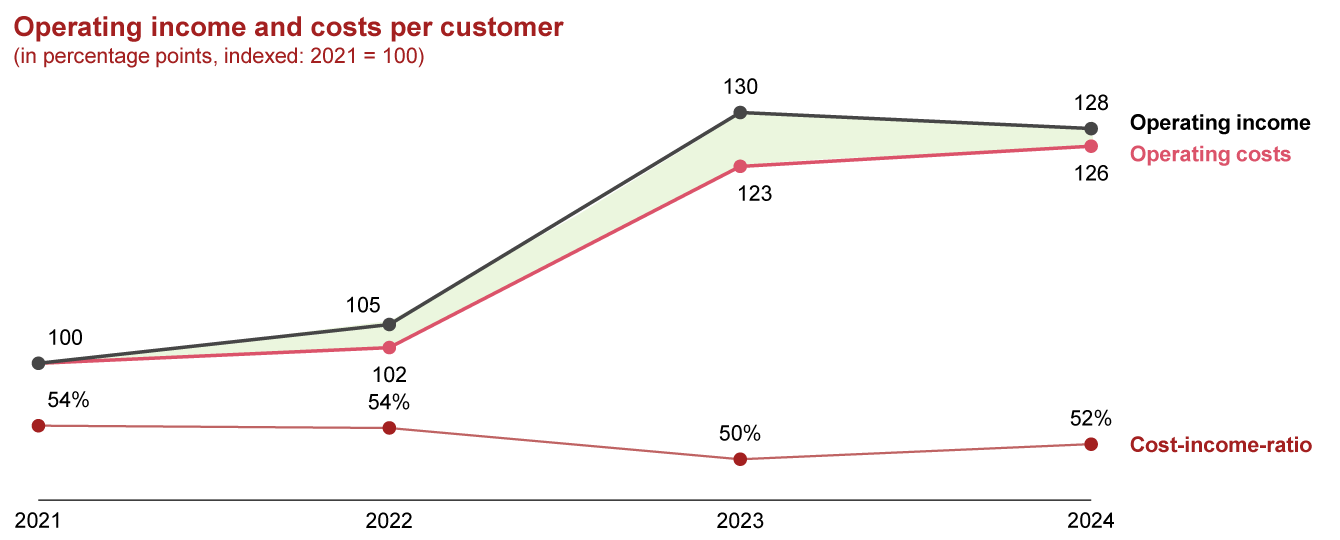

Compared to the record-breaking results of 2023, operating profit decreased by -5% y-o-y, driven by a combination of cost (+2% y-o-y) and volume of client increases, accompanied by a slight decline in revenues (-1% y-o-y). Despite this, Swiss banks maintained exceptionally high levels of profit and income, driven by elevated interest income as well as robust fees and commission income.

With steady customer demand and more favorable financing conditions, mortgages fueled the growth in loan volume (+3% y-o-y), while other loans experienced a slight decline. The beneficial interest rate environment resulted in strong net interest income per customer. Despite a decrease year-on-year (-4% y-o-y), it remains significantly elevated, standing +28% higher than in 2022.

On the horizon, nonetheless, there are signs for change. The four interest rate cuts by SNB in 2024, as well as one further cut in early 2025, signal a reversing of the trend that has buoyed Swiss retail banking interest income in the last two years. Of the banks in our sample who experienced sharp income decline, few had timed their interest responses differently to the SNB rate cuts.

Net fee and commission income per customer continued to grow in 2024, albeit at a more modest rate of 2% compared to the strong y-o-y increase of 11% in 2023. This sustained growth can be attributed to positive market developments bolstering management fees earned by banks, as well as increased customer activity, especially in ETFs and bonds.

But with significant macroeconomic uncertainty ahead (e.g., trade frictions, geopolitical conflicts), it appears unlikely that markets will be able to sustain the high valuations, putting commission income under pressure. Similar to their European peers, Swiss retail banks need to focus their topline strategy on generating sustainable commission income to cushion adverse market effects.

Cost did not follow the revenue trend and increased by +2% y-o-y, driven equally by personnel expenses and G&A expenses. No substantial prioritization of transformative cost-cutting initiatives was observed, despite high income levels:

Only a handful of banks in our sample, including three mid- to large-scale cantonal banks and two large banks, managed to reduce their operating costs per customer from 2023 to 2024. Meanwhile the Swiss branch network is slowly pursuing its policy of rationalization, at constant yearly rates of -1% to -2%.

The overall slight cost increase resulted in a 2% y-o-y rise in the cost-income ratio across Swiss retail banks to 52%, slightly higher than the European average.

The record years of 2023 and 2024 may have alleviated pressure to tackle persistent inefficiencies within the sector. The forecast for 2025 is less optimistic, with the combination of lower interest rates, potentially turbulent financial markets, challenging loan-to-deposit levels, and rise of challenger banks. Pressure on margins is to be expected, especially for incumbents who did not take advantage of the successful past years to transform.

Now is therefore an opportune moment for banks to embark on comprehensive operational transformations, focusing on cost management and process optimization (e.g., loan process digitalization, online onboarding) to ensure sustained competitiveness in the evolving financial landscape.

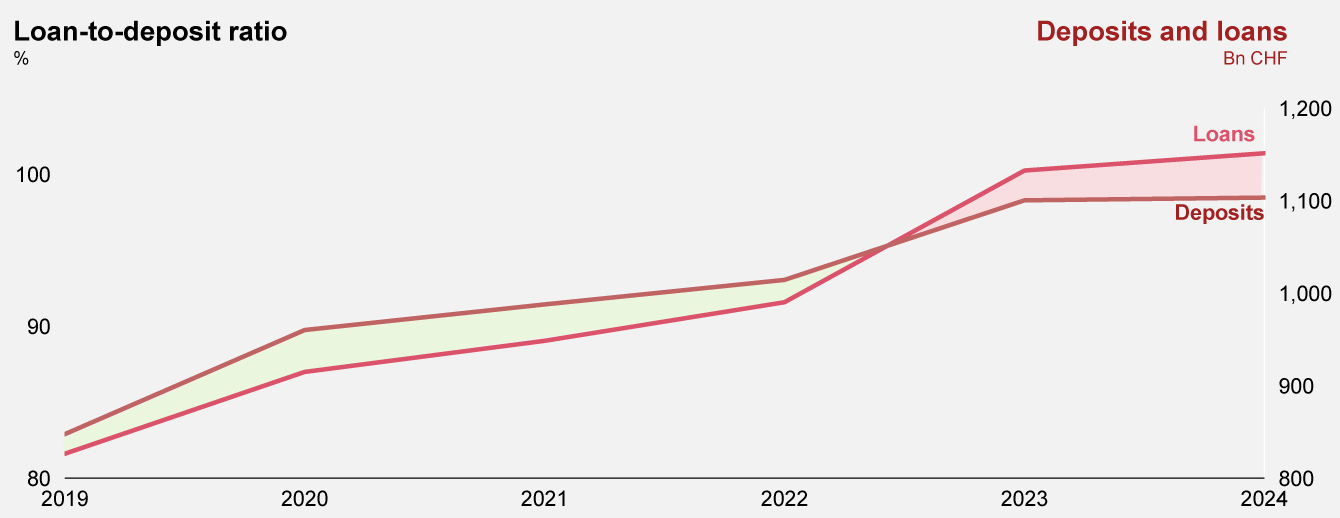

The trend in the loan-to-deposit ratio highlights the refinancing challenge Swiss retail banks are increasingly facing. The sharp uptick from 2022 to 2023 (98% to 103%) marked a shift by customers from current deposits into interest-bearing products and investments. 2024 confirms the new baseline (104%) to which banks must adjust.

No significant UBS/CS effects have been observed as yet on other Swiss retail banks’ customer base and deposit levels. Recent developments suggest that some cantonal banks within German-speaking Switzerland may have captured parts of the momentum.

Banks are being driven to explore alternative funding sources which come at a higher cost, such as bonds and central mortgage institution loans («Pfandbriefe»), as well as cash bonds («Kassenobligationen»). This exacerbates the pressure on net interest margins and overall profitability. Swiss banks must strategically adjust their balance sheet management and explore comprehensive solutions to mitigate the impact on their financial stability.

With interest rates decreasing, we do not expect the loan-to-deposit ratio to return to levels observed prior to 2022, but to pursue its current trend.

Swiss challenger banks have not yet reached a tipping point, despite their growth in recent years: The landscape is still fragmented, with low challenger bank penetration. Revolut is the largest challenger bank in Switzerland (~1m clients) and there are a few mid-size local players (e.g., Yuh, neon), with offerings focused on daily banking. A myriad of local niche challengers exist, mainly active as online brokers or robo-advisors around themed ETF offerings and/or digital 3a pillar products.

Other European countries were facing a similar scenario years ago and their situation has now evolved: local players are no longer niche players but true competitors capturing market shares (e.g., BoursoBank in France, Trade Republic in Germany, Starling Bank in the UK) and absorbing significant new customer growth.

Swiss incumbents should therefore not underestimate the potential of challenger banks, both local and foreign. We have observed initial adaptations from incumbents (e.g., BCF, Valiant, GKB) to offer free daily banking products or fully digital loans. Looking at the pressure in other European markets, there are further ways to act, with first movers likely to secure advantage.

The Strategy& Retail Banking Monitor provides a detailed analysis of the characteristics of successful challenger banks, as well as exploring how incumbents can adapt. Looking forward, we believe it is the following factors that will distinguish high-performing incumbent retail banks from challengers:

Traditional banks need to innovate to enhance their efficiency and attract the digital-savvy customer base that challenger banks are increasingly capturing.

Incumbent banks must expand their offerings to include lifestyle products, ensuring they stay relevant and competitive in the marketplace.

Traditional retail banks should reconsider their balance sheet strategies, exploring balance-sheet-light models to optimize profitability.

To address declining interest margins, traditional banks need to boost their fee and commission income through enhanced monetization strategies.

Incumbent banks should leverage their scale and established trust to effectively meet the diverse demands of the market.

Partner, Lead Strategy & Transformation, PwC Switzerland

Partner, Deals Financial Services, PwC Switzerland

Director, Strategy& Germany